Listen to this Recap

8:35

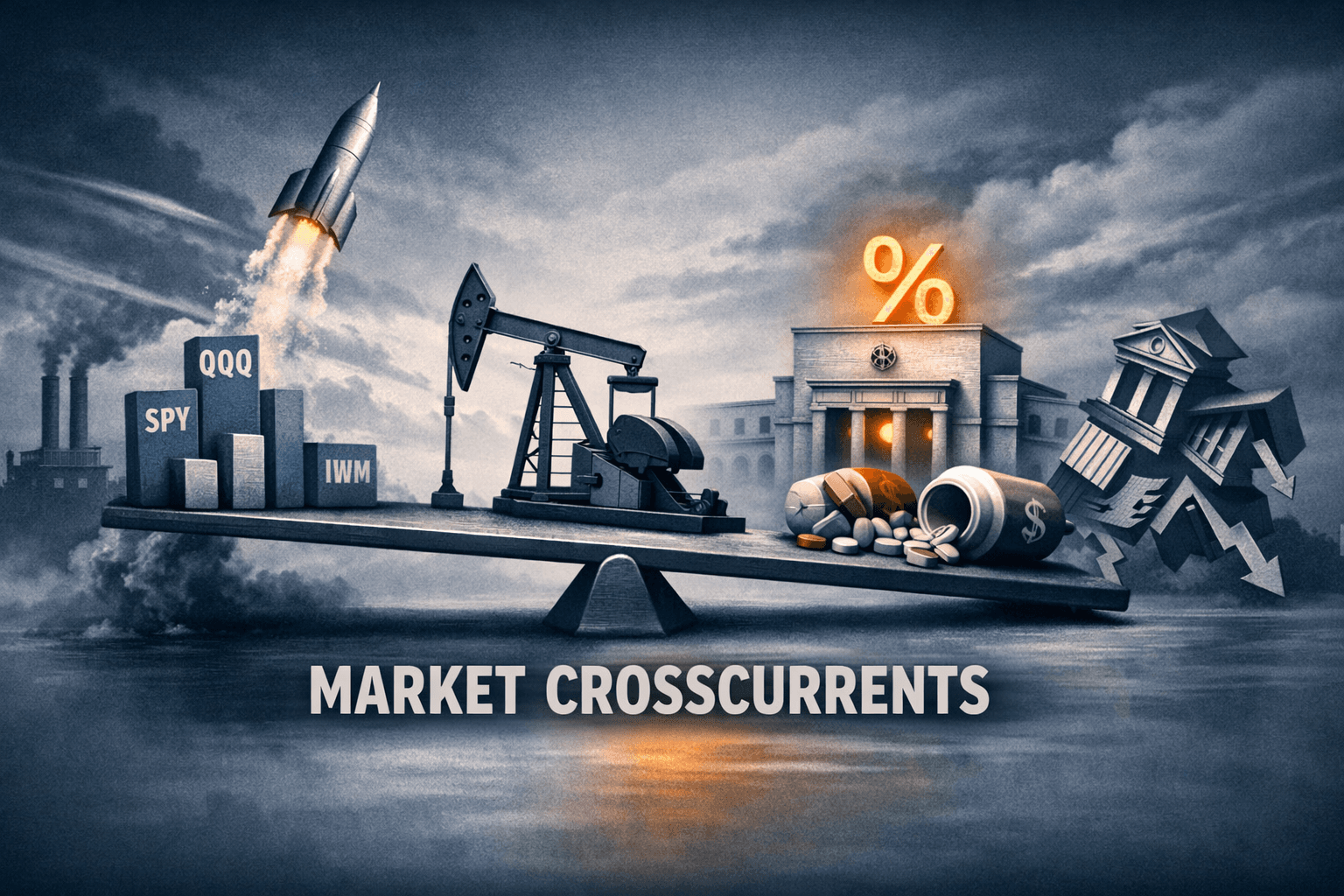

Tech-Led Rally Meets Macro Crosswinds: QQQ Outpaces as Small Caps Lag; Oil and Fed Signals Steal Spotlight

Podcast • Loading audio...

Share this article

Spread the word on social media

Key Takeaways

- •QQQ outperformed with an estimated +0.9% gain while SPY rose about +0.4% and IWM lagged at roughly -0.6%.

- •Tech and mega-cap growth led the market; narrow breadth underscores concentration risk.

- •Energy and materials saw momentum on an oil uptick, creating sector-specific leadership despite financials and small-cap weakness.

- •Notable stock moves: FedEx and MGM were among the day’s winners; Regeneron disappointed after trial results; JPM faced scrutiny.

- •Next session hinges on earnings cadence, commodity moves, and any inflation or Fed-relevant data that could shift rate expectations.

Decisive Market Narrative

The market's story on July 13 was one of concentrated strength and selective weakness: the Nasdaq-100 led the way while the broader market eked out modest gains and small-cap stocks lagged. The S&P 500 ETF (SPY) closed up an estimated +0.4% while the tech-heavy Nasdaq-100 ETF (QQQ) advanced roughly +0.9%. Small-cap pressure was evident as the Russell 2000 ETF (IWM) finished the day down about -0.6%.

That split — tech and large-cap leadership alongside small-cap underperformance — set the tone. Investors rotated toward a handful of growth and tech names tied to AI momentum and away from riskier late-cycle plays, even as energy and materials showed pockets of strength on an oil rebound. The resulting market profile was bullish for mega-cap growth, cautious across cyclical exposure, and sensitive to any macro or geopolitical headline that could influence rates and margins.

Why the Market Moved: Drivers Behind the Day

Several cross-currents explain today's market action.

Earnings positioning and lofty expectations: Analysts and traders highlighted that Wall Street's earnings expectations remain elevated, and that dynamic pushed volatile repositioning into perceived 'earnings safe' large-cap tech names and away from smaller, earnings-sensitive companies.

Commodity and energy strength: A notable pickup in oil prices and renewed interest in energy-sector names lent leadership to the energy and materials groups, supporting pockets of the rally despite broad market caution.

Risk signals in finance: Headlines flagged rising risk indicators in the financial sector — including increased scrutiny of bank leadership and regulatory questions — which weighed on financials and small caps more broadly.

Sector-specific news: Company-specific catalysts such as robust results from FedEx, multi-factor support for MGM Resorts, and disappointing clinical news from Regeneron created divergent stock moves that influenced sentiment unevenly.

Together, these elements produced a tape that rewarded concentration in large-cap tech and select cyclical plays tied to commodities, while punishing smaller, more economically sensitive names.

Index Performance (Early Summary)

- SPY (S&P 500 ETF): +0.4%

- QQQ (Nasdaq-100 ETF): +0.9%

- IWM (Russell 2000 ETF): -0.6%

These moves appeared early and defined the session: leadership centered in large-cap tech and growth, with breadth narrower than the headline gains suggested.

Sector Rotation and Standout Performers

Sector action was uneven and thematic.

Technology/Communications: Tech again took center stage, driven by AI-related narratives and several favorable earnings previews. The communications and media complex showed mixed signals, but the overall technology-centric indices outperformed.

Energy: An oil surge provided a lift to energy stocks and related industrial names. Renewed geopolitical or supply concerns and stronger commodity demand pushed energy to one of the day's top sectors.

Materials & Industrials: Materials and industrials saw momentum as mining and commodity-related firms responded to firmer commodity prices. Manufacturing and industrial news also contributed to selective gains.

Utilities & Renewables: Utility names, especially renewables, had pockets of momentum as investors rotated into defensive yield-plus-growth names amid persistent rate uncertainty.

Financials: Finance showed stress signs. Headlines about JPMorgan leadership scrutiny and broader risk indicators undercut the sector, contributing to small-cap weakness given the sector's weighting in IWM.

Real Estate: Activity remained mixed — deals and distress narratives created volatility for the group, with some REITs seeing selling pressure while others rallied on deal announcements.

Overall, the rotation favored growth-and-commodity exposures over beaten-down cyclical small caps, producing the divergence between QQQ and IWM.

Key Economic Data and Fed Implications

Macro was a silent but influential hand. While no jaw-dropping economic release landed during the session, market participants are clearly positioning for tighter-than-expected policy risks.

Inflation sensitivity: The energy-led uptick in commodity prices raised concerns that inflation pressures could reassert themselves, which would complicate the Federal Reserve's outlook. Traders noted that renewed energy strength can feed through to headline inflation in coming months.

Fed-watch dynamics: With earnings expectations still elevated and risk indicators in finance increasing, the Fed narrative remains a central input. Analysts note that sustained commodity-led inflation pressures would likely keep the Fed on a higher-for-longer script, while any signs of economic slowing could dampen that view. For now, positioning reflects a wait-and-see stance but with heightened sensitivity to incoming CPI/PCE readings and Fed speeches.

Market pricing: Treasury yields moved in sympathy with risk flows, and volatility in financials and small caps suggests traders are trading around policy risk rather than expecting a clear pivot.

All told, data and macro narratives suggest markets remain reflexive to inflation and rate trajectories; even sector-specific moves are being read through the lens of Fed implications.

Notable Individual Stock Moves

FedEx (FDX): Reported what analysts called robust results and a clearer focus on operational discipline. The print supported industrial and logistics names and was cited as evidence of margin recovery in parts of the transport sector. FDX was one of the day’s top performers after the update.

MGM Resorts (MGM): Multiple factors — from better tourist flows to optimistic margin commentary and favorable gaming metrics — lifted the stock, contributing to leisure and consumer discretionary strength in selective names.

Regeneron (REGN): Disappointing trial results for a key program weighed on the biotech name and rippled across the healthcare sector. Regeneron's setback was the standout negative among large-cap healthcare stories and prompted profit-taking in several drug developers.

Micron (MU) and UnitedHealth (UNH): Both were highlighted in earnings/coverage notes as companies to watch. Micron in particular has been emblematic of AI-related demand narratives, and momentum related to memory cycles supported chip-related names.

JPMorgan (JPM): The bank faced heightened scrutiny after high-profile questioning of its leadership, which, combined with broader finance risk signals, pressured the stock and the financial sector generally.

Euronet Worldwide (EEFT): Coverage and analyst debate left sentiment mixed; the name featured in day-specific research discussions and saw above-average activity.

These moves exemplified the day's selective, name-by-name market behavior rather than broad sector uniformity.

Technical and Market-Structure Notes

Technically, the tape looked like a classic large-cap-led rally with narrowing breadth. QQQ's outperformance suggests momentum remains concentrated in a small group of mega-cap growth stocks. Momentum indicators suggest resistance tests at recent highs; traders will watch for follow-through volume. Conversely, IWM’s underperformance implies risk-aversion among smaller capitalizations and could signal relative weakness in cyclical and value exposures if the trend persists.

Option flows and positioning ahead of major earnings and macro prints are likely contributing to compressed volatility in some large names while amplifying moves in smaller, news-driven stocks.

Outlook — What to Watch Next Session

Heading into the next trading day, market participants will be watching a compact list of items that could tip the balance:

Macro prints: Any incoming inflation or labor data will be parsed for Fed implications. Even minor upside surprises on inflation could reprice rate expectations and weigh on rate-sensitive sectors.

Earnings cadence: High-profile earnings and guidance from mega-cap techs and cyclical bellwethers will set the tone. Given how elevated expectations are, companies’ forward commentary will matter as much as headline numbers.

Commodity moves: Further moves in oil and base metals could reaffirm rotation into energy and materials or, alternatively, prompt risk-off if those moves are interpreted as inflationary.

Financial sector headlines: Any follow-up on banking risk indicators or regulatory developments could exacerbate the small-cap underperformance and pressure regional and payment names.

Technical action: Watch SPY/QQQ levels for intraday follow-through — sustained breadth improvement would be a constructive sign, whereas continued narrow leadership would caution that rallies remain fragile.

In short, the next session is likely to be defined by macro sensitivity and earnings-driven dispersion, with investors balancing AI-and-growth enthusiasm against rate and commodity risks.

Historical Context

This pattern — narrow, tech-led gains with small-cap weakness — has recurred in prior cycles where liquidity and sentiment concentrate in visible growth leaders while the broader economy shows mixed signals. Historically, sustained market advances require breadth improvement; if breadth does not broaden in the coming sessions, similar rallies have tended to stall or become volatile corrections. That does not preordain outcomes, but it frames why traders are watching both sector rotation and breadth closely.

Investment Disclaimer

This report is for informational purposes only and does not constitute investment advice. Analysts note market data and commentary reflect observed price action and publicly available information. No recommendation to buy, sell, or hold any security is being made. Readers should consult their own financial advisors for personalized guidance.

Bottom Line

July 13's market action underscored a bifurcated landscape: technology and select large caps carried the tape while small caps and financials showed cracks. Commodity-led pockets of strength added nuance, creating an environment where macro data, earnings commentary, and Fed implications will likely dictate whether the narrow leadership broadens into a durable advance or remains a fragile, concentration-driven move. Traders and longer-term allocators alike should watch breadth, inflation signals, and earnings updates closely for the next directional clues.

Sources

+ 10 more sources

Use these insights — enter this week's contest.

Free practice contests — earn Alpha CoinsExplore More Content

Disclaimer: StockAlpha.ai content is for informational and educational purposes only. It is not personalized investment advice. Sentiment ratings and market analysis reflect data-driven observations, not buy, sell, or hold recommendations. Always consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.