Listen to this Recap

9:24

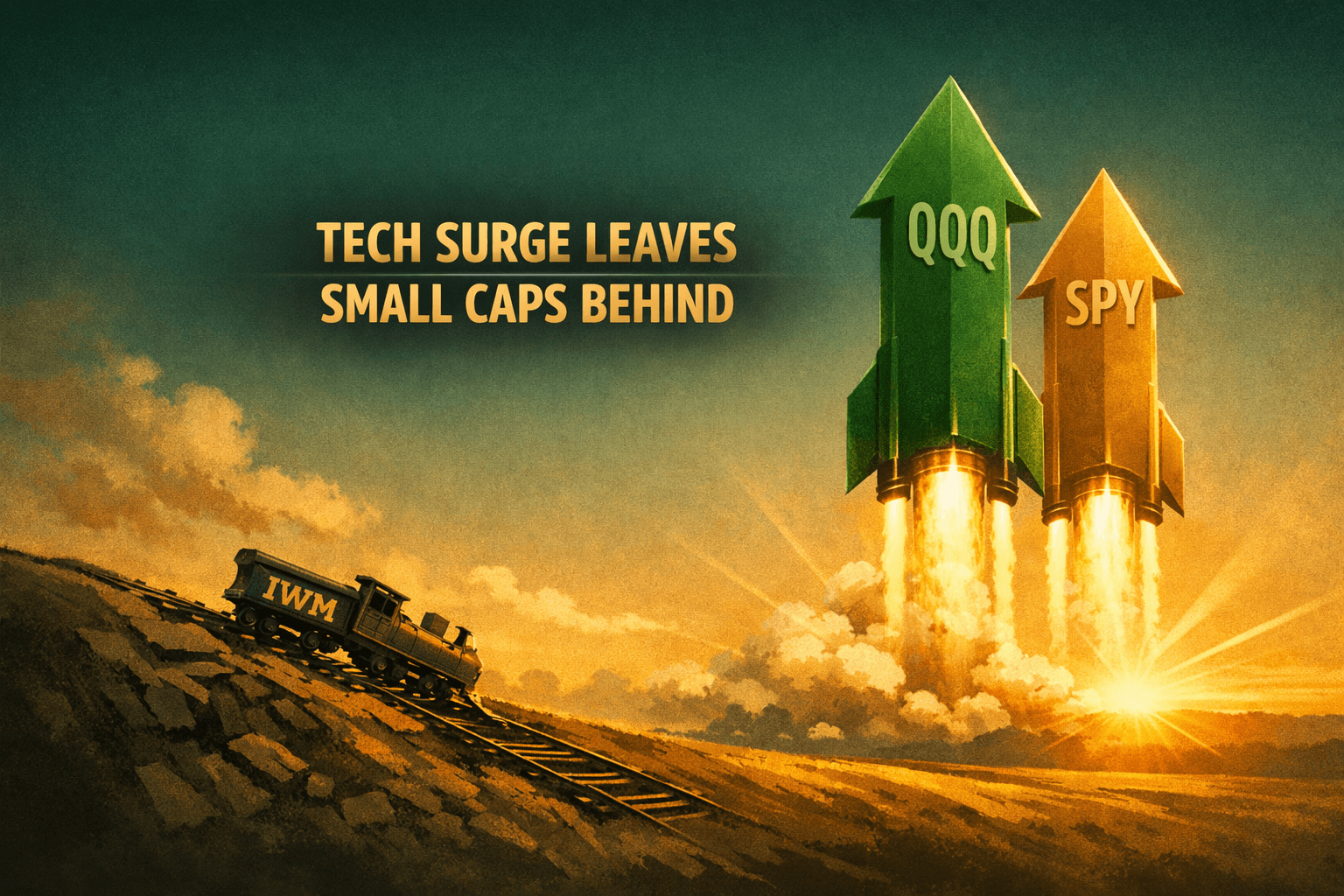

Tech-Led Rally Sends Benchmarks Higher as Small Caps Lag: SPY +1.65%, QQQ +2.49%

Podcast • Loading audio...

Share this article

Spread the word on social media

Key Takeaways

- •Large-cap tech leadership drove gains: SPY +1.65% and QQQ +2.49%, while small caps lagged with IWM -0.29%.

- •Rally breadth was narrow — gains concentrated in mega-cap growth, raising sustainability questions without broader participation.

- •Energy, materials and utilities showed pockets of strength on rising oil prices and renewables momentum.

- •Earnings beats (e.g., RPRX, EQIX) and analyst support helped fuel selective moves; Fed and inflation trends remain central to direction.

- •Watch Russell 2000 performance, upcoming macro prints and further earnings for signs the rally is broadening or staying top-heavy.

Market snapshot: Mega-cap strength, narrow breadth

The market’s clearest message Thursday was concentration: big-cap tech led a broad-market pop while smaller stocks trailed. The S&P 500 (SPY) closed up 1.65% while the tech-heavy Nasdaq-100 (QQQ) surged 2.49%. Small caps underperformed, with the Russell 2000 (IWM) down 0.29%, underscoring that today’s rally was driven by a subset of large-cap names rather than broad risk-on flows.

That split — outsized gains in large-cap growth and a modest decline in small-cap stocks — framed trading all day. Headlines around rescheduling momentum in cannabis, stronger oil prices and several upbeat corporate updates helped, but the most forceful narrative was renewed appetite for AI and megacap earnings momentum that concentrated gains at the top of the market.

Why the market moved: leadership, narratives and fundamentals

Several overlapping themes explain the move:

- AI and mega-cap leadership: Continued enthusiasm for AI and cloud resilience pushed gains in the Nasdaq-100, with investors rotating into high-margin, durable-growth names. Analyst notes and institutional support — including continued favorable posture from major banks — reinforced momentum.

- Earnings and company-specific beats: A string of results and company updates mattered. Royalty Pharma (RPRX) rallied after an earnings beat, while Equinix (EQIX) drew attention for multiple factors lifting its Q1 narrative. Those reports removed some near-term earnings uncertainty and helped validate growth narratives at the top end of the market.

- Energy tailwinds: Rising oil prices lent a tailwind to energy names and to broader cyclicals tied to commodities and industrials. Chevron’s Q1-led surge was emblematic: higher commodity prices and stronger cash-flow narratives supported the group.

- Persistent inflation concerns: Surveys continue to show inflation remains a top worry for Americans. That macro backdrop keeps the Fed’s policy path in focus and underpins the tilt toward large-cap franchises with perceived pricing power.

Sector rotation and standout performers

Although the index moves give a bullish headline, sector action was more nuanced:

- Technology / Communications: The standout sector was technology and large-cap communication services. QQQ’s outperformance shows investors favored software, semiconductors and cloud businesses tied to AI and secular growth. Communications and media delivered mixed signals — some names spiked on structural narratives, others reflected profit-taking after recent gains.

- Energy: Energy enjoyed a solid session as oil prices rose. Chevron’s strength typified the group’s response to stronger commodity dynamics and helped underpin parts of the S&P rally.

- Utilities: Utilities showed momentum linked to renewables narratives. Defensive exposure that also benefits from long-term green infrastructure spending found buyers as part of a trade balancing growth exposure.

- Materials & Mining: Materials saw momentum related to industrial demand and commodity flows — miners and specialty chemicals joined the move as investors priced in supply-demand improvements.

- Real Estate: Activity in real estate was notable for deal flow and development stories, not broad re-rating. Certain REITs rallied on M&A or development headlines, but the sector’s performance remained mixed overall.

- Financials & Insurance: The finance complex was mixed. Selective Insurance (SIGI) was in the spotlight with analyst coverage updates; life insurers like Globe Life (GL) saw discussion around Q1 performance. Banks didn’t broadly lead despite some upbeat notes from sell-side firms.

- Small Caps: Underperformance in IWM highlighted risk-off among smaller, more economically sensitive names even as large caps advanced.

Notable individual movers (high level)

- Equinix (EQIX): Multiple factors lifted the company’s Q1 takeaways, combining solid demand for data centers and favorable secular trends tied to cloud expansion.

- Royalty Pharma (RPRX): The stock rallied on an earnings beat and stronger-than-expected guidance/metrics for the quarter.

- Chevron (CVX): Rising oil prices and Q1 commentary drove a sharp move higher for this major energy name.

- Selective Insurance (SIGI), Jacobs Solutions (J), Globe Life (GL), Mediaalpha (MAX): These mid- and small-cap names drew analyst attention and rating updates; the coverage created intra-day volatility across financials, industrials and media.

Note: The session featured many company-specific analyst notes and sector updates that moved individual names. Analysts’ coverage (buy/sell/hold reassessments) and Q1/quarterly commentary were frequently catalysts in otherwise headline-driven trading.

Macro, inflation and Fed implications

Inflation remained the elephant in the room. Survey data reiterated that inflation is Americans’ top financial concern; that persistent sentiment keeps the Federal Reserve’s policy path front-and-center for markets. Several implications flowed from that reality:

- Policy sensitivity: With inflation concerns still elevated, investors continue to price Fed credibility and the chance of slower cycles of rate relief. That dynamic helps explain why large-cap tech — companies perceived as having pricing power and long-duration cash flows tied to secular growth — outperformed.

- Value vs. growth tension: Historical patterns show value tends to beat growth in high inflation regimes. Today’s action deviated from that historical tendency as growth stocks, especially AI-exposed and software names, outperformed. That suggests the market is currently giving incremental weight to technology-driven productivity and margin expansion over classical inflation rotation.

- Market expectations: Fed communication, upcoming inflation prints and labor-market data remain the next big drivers. Traders are watching for any signs that inflation is finally on a sustainably downward trajectory; absent that, premium valuations for growth names could remain under scrutiny even as they rally in the near term.

Technical and breadth read

Technically, the tape showed classic narrow participation: the major indices climbed, but breadth was weak because gains concentrated among the largest-cap names. That pattern raises two key flags for traders:

- Rally quality: A rally led by a handful of mega-caps is inherently more fragile than one supported by broad-based participation. Market breadth metrics remain worth watching; if breadth doesn't improve quickly, the risk of a chop or pullback increases.

- Support and momentum: Momentum indicators favored the winners today, and a number of large caps cleared near-term resistance levels. That technical clearance can attract momentum flows, but sustainability depends on follow-through from mid- and small-cap participation.

Cryptocurrency and risk assets

Cryptocurrency signals were mixed: digital-assets volatility persisted and gave a mixed contribution to risk appetite across macro and equities desks. Crypto activity is not yet behaving as a consistent risk-on proxy; instead it appears as an independent asset class with episodic spillovers into broader sentiment.

What this means for tomorrow (the near-term outlook)

- Watch breadth and IWM: If the Nasdaq keeps its pulse but IWM remains weak, the market will be vulnerable to a pullback if leadership narrows further. Traders should watch Russell 2000 flows for confirmation of broad-based risk appetite.

- Earnings and analyst notes: Continued company-level headlines — especially additional beats or guidance raises — could keep a bid under growth names. Conversely, any major disappointments will be magnified given today’s concentration.

- Macro calendar and Fed speak: With inflation still a dominant investor worry, incoming CPI/PPI prints and Fed-speak will move markets. Any signs of stickier inflation or hawkish tilt from Fed officials would likely favor defensive sectors and reintroduce pressure into high-valuation growth names.

- Commodity and energy moves: Oil prices remain a key input for cyclical and energy sector returns. A continued rise would keep energy stocks in leadership and support related cyclicals; a quick reversal would tighten market textures.

Historical context and how to interpret this rally

Narrow leadership has precedence. Several multi-year rallies began with concentrated leadership (tech or cyclical) before breadth broadened — and several corrections began the same way. What matters now is confirmation: sustained breadth expansion and participation from mid- and small-caps would validate a durable bull phase; continued narrow leadership increases the chance of choppy returns and elevated volatility.

Bottom line

Thursday’s session rewarded mega-cap, AI-linked names and left small caps behind. SPY’s 1.65% rise and QQQ’s 2.49% surge were strong headline moves, but IWM’s 0.29% decline is an important reminder that today’s strength was not uniform. Energy, materials and utilities showed pockets of reason for optimism as commodity and renewable narratives continued to attract flows, while corporate beats and analyst support amplified interest in select large-cap names.

Investors and traders should watch breadth, upcoming macro prints and continuing earnings flow to judge whether this rally broadens or remains top-heavy. The market is acting bullishly today, but the narrow participation pattern keeps the path forward contingent on confirmation from a wider universe of stocks.

Disclaimer

This report is for informational purposes only and does not constitute personalized investment advice. The analysis reflects market data and commentary available at the time of writing. Analysts note trends and risks, and share observations about market dynamics — not specific buy, sell, or hold recommendations.

Sources

+ 10 more sources

Use these insights — enter this week's contest.

Free practice contests — earn Alpha CoinsExplore More Content

Disclaimer: StockAlpha.ai content is for informational and educational purposes only. It is not personalized investment advice. Sentiment ratings and market analysis reflect data-driven observations, not buy, sell, or hold recommendations. Always consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.