Listen to this Recap

8:29

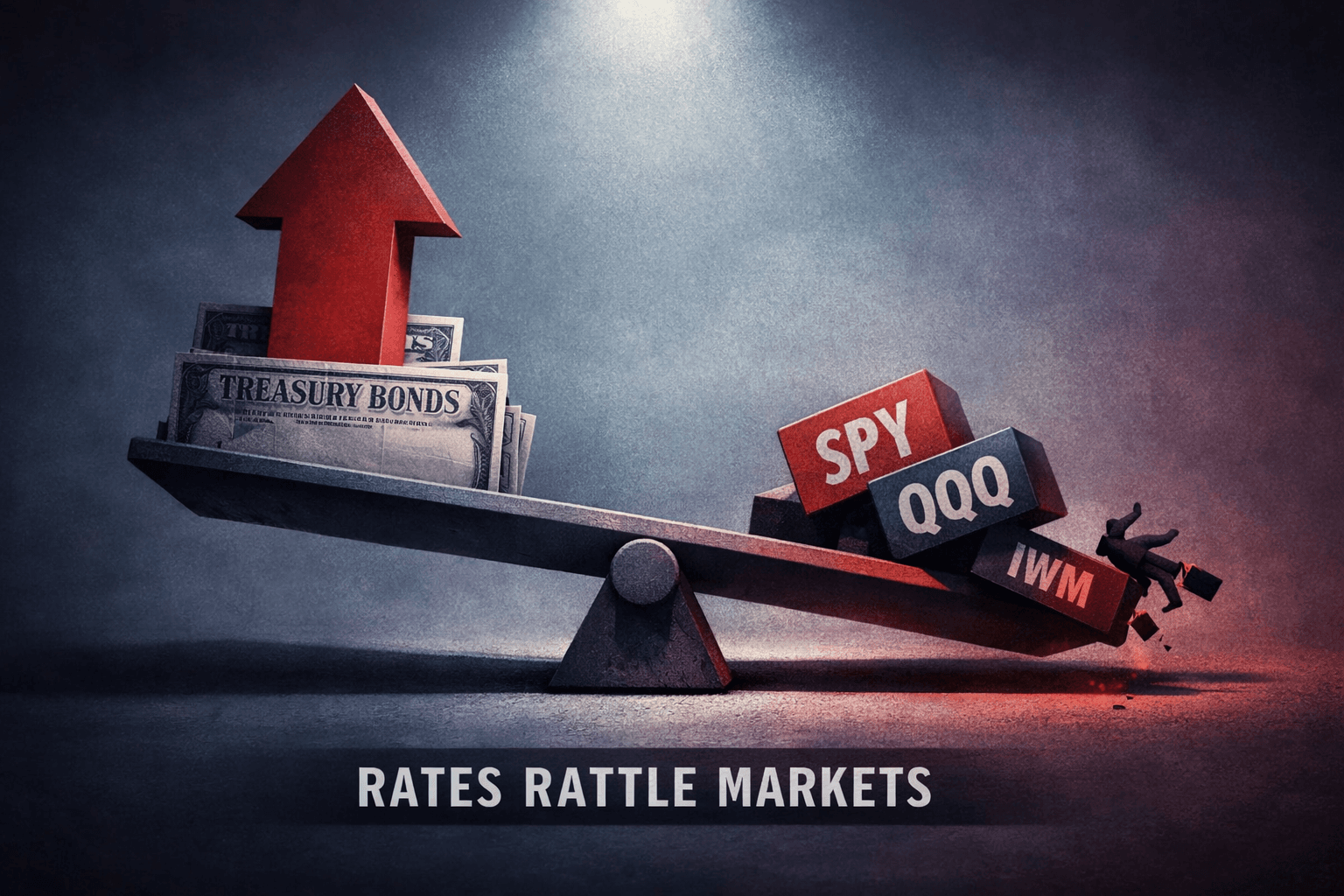

Risk-Off Mood as Yields Rise: SPY, QQQ Fall; Small Caps Underperform on Rate Jitters

Podcast • Loading audio...

Share this article

Spread the word on social media

Key Takeaways

- •SPY closed down -0.67% and QQQ fell -0.62%; small caps (IWM) lagged with a -1.08% decline.

- •Rising long-term yields (30-year > 5.19%) were the primary driver, tightening financial conditions and pressuring rate-sensitive names.

- •Sector dispersion: renewables, materials and select consumer names held up while financials and small caps showed mixed to negative performance.

- •Company-level headlines (Nvidia, HPE, Home Depot, AT&T, Evertec) created idiosyncratic moves amid the broader risk-off tone.

- •Monitor Treasury yields, Fed communications, housing data and upcoming earnings for clues to the next directional leg.

Today's decisive narrative

The market moved into a risk-off posture on May 19 as rising long-term Treasury yields and mixed macro and corporate news combined to sap risk appetite. The S&P 500 ETF (SPY) closed down -0.67% while the tech-heavy Nasdaq-100 ETF (QQQ) slipped -0.62%. Small caps underperformed more visibly, with the Russell 2000 ETF (IWM) down -1.08% — a signal that investors rotated away from higher-beta, economically sensitive names into perceived safety or defensive sectors.

The move reflected a cross-current market: pockets of strength in renewables, materials and select consumer names were outweighed by broader rate-related pressure, headline company developments and continued sector dispersion. With the 30-year Treasury yield topping 5.19% during the session, fixed-income moves were central to equity dynamics today.

How we got here: bond yields, economics and Fed implications

The most consequential backdrop was the rise in long-term yields. The 30-year Treasury climbing above 5.19% tightened financial conditions and raised the cost of capital for growth and long-duration assets. Historically, sustained increases in long-term rates put pressure on mega-cap growth multiples; today's intraday behavior echoed that pattern as QQQ performed only marginally better than the broader S&P but still finished negative.

What this means for the Fed picture: markets are pricing a slower path to rate cuts than had been hoped for earlier in the year. While the Federal Reserve has signaled that it will closely watch incoming data, higher long-term yields imply less room for immediate easing. Analysts note that if inflation measures and labor data remain firm and yields stay elevated, the Fed may pause on easing or move later than markets previously anticipated.

The implication for real estate and housing is immediate: mortgage rates track long-term yields, and a 30-year near or above 5% weighs on housing affordability and refinance activity. That dynamic connects to today's real estate commentary around deal flow and development, which showed mixed momentum.

Sector rotation and notable sector moves

Utilities and renewables: Utilities drew interest on a combination of defensive flows and sector-specific momentum in renewables. The utilities wrap indicated that clean-energy investments and renewable project pipelines are supporting selective strength, even in a risk-off session.

Materials & Mining: The materials complex showed resilience, driven by lithium and copper interest. Reports of Q1 wins and ongoing demand for battery metals supported names exposed to EV supply chains and industrial electrification.

Energy: The energy sector was bifurcated — Europe-facing energy names were hit by regional headwinds while renewables-focused energy companies found buying interest, reflecting longer-term structural demand for clean power.

Communications & Media: The communications and media space was active, with content trends and capex plans prompting rotation into more defensive or cash-generative names amid a cautious tape.

Financials: Finance and banking displayed mixed signals. Some banks met investor expectations while others wrestled with margin pressure as yields rose on the long end but bank funding dynamics remained nuanced.

Consumer & Retail: Consumer and retail showed pockets of momentum, with select retailers reporting encouraging comparable sales trends that kept parts of the discretionary complex afloat despite the broader pullback.

Small caps: IWM's -1.08% decline underscores the day's small-cap weakness — a common response when investors price in a more uncertain economic outlook and prefer large-cap liquidity and balance-sheet strength.

Individual-stock headlines that moved markets

Nvidia (NVDA): Nvidia remained in the spotlight after HSBC raised its price target, a bullish signal for the semiconductor heavyweight and the broader AI-related trade. Analysts say the upgrade provided intraday support for semiconductor peers, even as the tech-heavy QQQ finished lower.

Hewlett Packard Enterprise (HPE): HPE traded down on the day amid specific company commentary and earnings-related digestion. Hardware and enterprise tech remain sensitive to capex cycles and macro guidance.

Home Depot (HD): Chart watchers tracked Home Depot following Q1 comparable-sales data. The reading fueled debate over home improvement demand in the context of higher mortgage rates and what that means for housing-related retail.

AT&T (T): AT&T's post-Q1 assessment prompted analyst discussion about telecom fundamentals, balance-sheet priorities and dividend sustainability, themes that factor into the communications sector's performance.

Evertec (EVTC): Post-Q1 positioning and analyst coverage sparked a re-evaluation of the payments processor's outlook, with mixed opinions on growth trajectory and margin leverage.

Granite Construction (GVA): Coverage highlighting reasons investors favor Granite Construction drew attention to construction and infrastructure exposure amid public and private investment cycles.

Deutsche Bank commentary: Analysts weighed geopolitical comments from Deutsche Bank that suggested the Iran conflict lacked certain escalation drivers, a note that reduced tail-risk premium for some energy-related assets.

Other micro headlines — a political anecdote comparing Nancy Pelosi to Warren Buffett and analysis on how oil shocks have historically affected markets — added to the narrative mix, reminding investors of the variety of fundamental and narrative drivers in play.

Cryptocurrency and alternative assets

Crypto markets sent mixed signals today. Some participants pointed to idiosyncratic flows and profit-taking after recent rallies, while others cited continued institutional interest in certain tokens. Mixed crypto performance often feeds into equity risk appetite, especially for risk-on cyclical names and thematic allocations tied to digital assets.

Technical and market-structure observations

Breadth: The divergence between the moderate drops in SPY and QQQ and the larger decline in IWM suggests breadth deterioration — fewer stocks participated in any intraday bounce, and small-cap weakness signaled risk-off breadth.

Sector leadership: Defensive leadership (utilities, select consumer staples) amid rate-driven pressure on growth supports a tactical shift toward lower-volatility names in the near term, according to technical momentum indicators.

Support/resistance: Market participants are watching key support levels in SPY and QQQ (near recent swing lows) — a break below these could invite a deeper correction, whereas a stabilization and a retreat in yields would likely re-energize growth leadership.

What to watch next (outlook for the next session)

Treasury yields and the curve: Continued moves in the 10- and 30-year Treasury yields will be the single most important market input. A sustained drop in yields would relieve pressure on growth and small caps; additional upward moves will likely keep a lid on risk assets.

Fed speakers and economic releases: Any comments from Fed officials or fresh inflation/employment data will be parsed for clues on the timing of rate cuts. Markets will watch for signals that the Fed is less likely to ease quickly.

Earnings cadence and company-specific reports: With a steady stream of corporate updates still coming, headline earnings guidance or capex commentary (especially from large-cap tech, industrials and consumer names) can quickly tilt sector leadership.

Housing and credit-sensitive data: Given the 30-year yield move, housing starts, existing home sales and mortgage application trends will be important for the real-estate and home-improvement ecosystems.

Geopolitical and commodity-linked headlines: Energy flows, supply-chain updates and geopolitical risk continue to create episodic volatility, particularly for energy, materials and industrials.

Traders should be prepared for continued dispersion and selective opportunities as the market digests the competing forces of higher long-term rates and sector-specific fundamentals. Analysts note that any decisive reversal in yields or a clear Fed communication pivot could rapidly change the leadership backdrop.

Historical context and framing

Today's action is reminiscent of prior periods when long-dated yields re-priced higher amid resilient economic data or shifts in inflation expectations. In those episodes, small caps and long-duration growth stocks corrected more sharply while value-oriented and defensive sectors outperformed. Momentum indicators and breadth often provided the early warning signs of a rotation; today's IWM underperformance fits that historical pattern.

Bottom line

Markets closed lower across major ETFs: SPY -0.67%, QQQ -0.62% and IWM -1.08%. The driving theme was rate sensitivity — specifically, rising long-term Treasury yields — layered on a mixed set of sector and corporate news. Renewables, materials and select consumer names showed pockets of strength, while small caps and certain tech and hardware names struggled. Going into the next session, yields, Fed communications, housing data and earnings releases will be the primary market movers.

Investment disclaimer: The information in this report is for informational purposes only and does not constitute investment advice or a recommendation to buy, sell or hold any security. Analysts note market momentum and data trends, but this is not personalized investment guidance.

Sources

+ 10 more sources

Use these insights — enter this week's contest.

Free practice contests — earn Alpha CoinsExplore More Content

Disclaimer: StockAlpha.ai content is for informational and educational purposes only. It is not personalized investment advice. Sentiment ratings and market analysis reflect data-driven observations, not buy, sell, or hold recommendations. Always consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.