Listen to this Recap

7:26

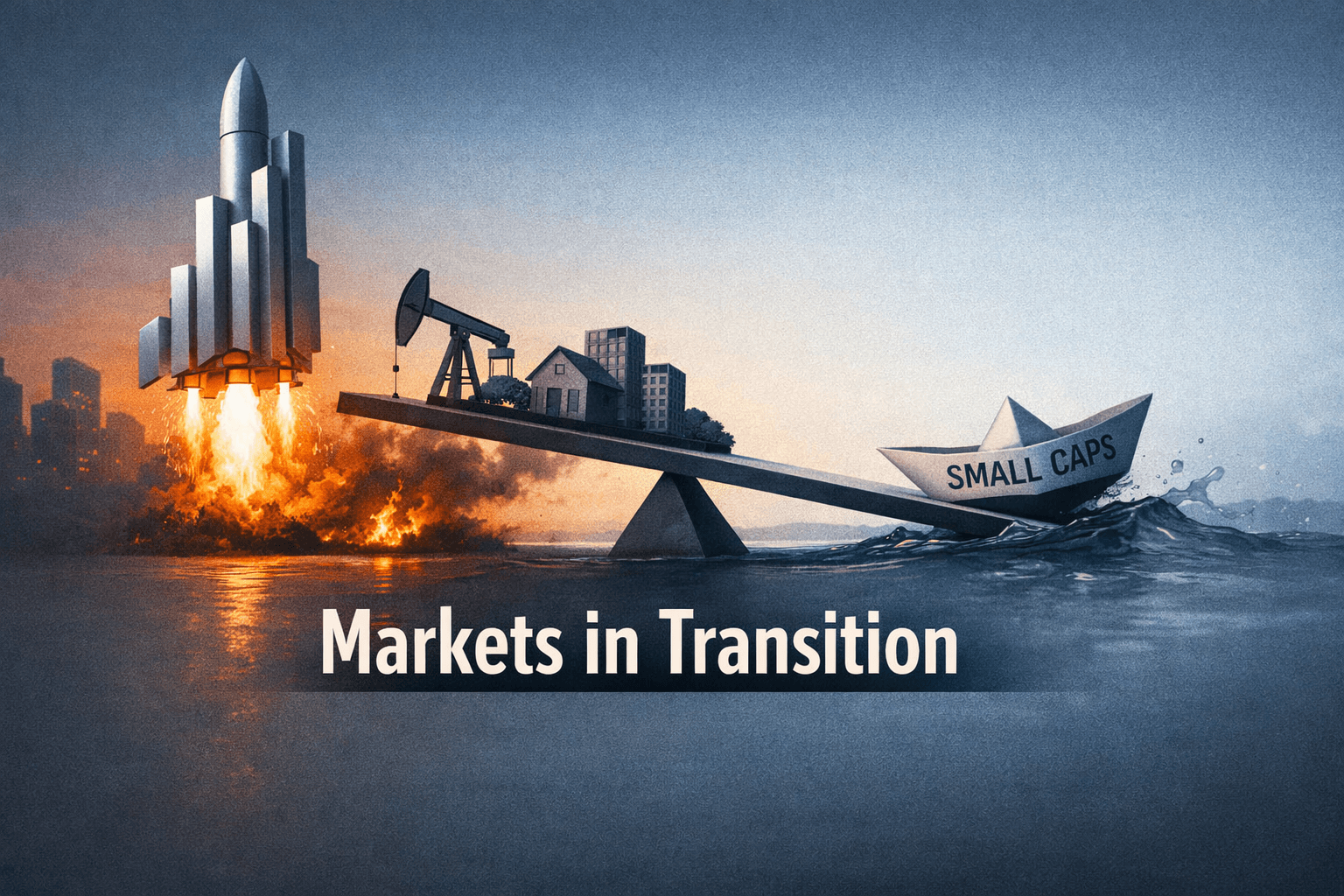

Megacaps Lift Nasdaq While Energy and Real Estate Drive Rotation; Small Caps Lag

Podcast • Loading audio...

Share this article

Spread the word on social media

Key Takeaways

- •QQQ outperformed with approximately +1.2% as megacap flow drove tech strength; SPY closed up about +0.6% while IWM lagged near -0.4%.

- •Energy and real estate showed the strongest sector performance—energy on a supply shock and real estate on deal activity.

- •Market breadth was narrow: concentrated megacap leadership leaves the rally vulnerable without broader participation.

- •Fed-watch: energy-driven inflation risks complicate the near-term Fed outlook; upcoming inflation and payroll data are key.

- •Next session focus: whether leadership broadens beyond megacaps, commodity trajectory, and any confirming earnings or deal updates.

Today's Decisive Narrative

Markets closed the day with a clear intra-market split: large-cap technology leadership contrasted with renewed strength in energy, materials and real estate, while small-cap and industrial weakness capped a mixed tape. The S&P 500 (SPY) closed up approximately +0.6% while the tech-heavy Nasdaq-100 (QQQ) advanced roughly +1.2%. Small caps lagged with the Russell 2000 ETF (IWM) down about -0.4%.

That dispersion — a QQQ-led upside alongside an IWM pullback — framed a session of cross-sector rotation rather than broad market breadth. Momentum flowed into a handful of sectors and megacaps, while cyclicals linked to manufacturing and small-cap domestic demand stayed under pressure.

Why the Market Moved: Flow, Fundamentals and Headlines

Several forces combined to produce today's pattern:

Energy supply shock and renewable-led action: a fresh round of supply concerns pushed oil and related energy names higher, lifting sector sentiment and commodity-linked stocks. The move had a two-fold market impact: it supported headline earnings expectations for energy firms and raised near-term inflation concerns, which in turn supported commodity-exposed sectors.

Real estate deal activity: a flurry of transactions and financing news in REITs and property-related names created pockets of strength, sending the real estate complex higher and attracting yield-seeking flows.

Megacap liquidity and rotation into depressed tech valuations: institutional activity and reported program flows involving major tech names helped QQQ outperform. Analysts and market participants noted renewed appetite for the largest cap names after extended periods of valuation compression.

Industrial and small-cap weakness: signs of slower manufacturing activity and subdued domestic demand pressure small-cap stocks, keeping IWM negative despite strength elsewhere.

Those dynamics produced a market that was selective rather than directional: leadership concentrated in a few sectors and megacaps, while the rest of the market waited for confirmation.

Sector Rotation and Standouts

Energy: The clearest sector winner. Supply-side headlines and tightening differentials pushed energy names higher. The rally was broad, covering integrated oil & gas as well as some energy services and select renewables names that trade as part of the broader energy/utility complex.

Real Estate: Deal-driven momentum lifted REITs and developers. Market participants cited several financing and M&A updates that underpinned optimism around balance-sheet improvements and yield arbitrage.

Materials & Mining: Project activity picked up, lifting miners and materials suppliers. The move looked partially driven by commodity price strength from energy and by incremental demand expectations tied to construction and industrial projects.

Utilities: A mixed picture. Utilities benefiting from storage momentum—both in the energy storage and regulated utility storage solutions—posted gains, while names tied to coal restarts saw pockets of volatility as markets recalibrated transition narratives.

Communications & Media / Cannabis: These sector-specific wraps showed idiosyncratic moves. Media and communications had selective strength tied to content and distribution announcements, while cannabis stocks continued to fluctuate on policy and retail-demand headlines.

Industrials & Manufacturing: Under pressure across the board. Names tied to heavy manufacturing and global trade showed weakness as activity indicators pointed to softer demand and inventory adjustments.

Financials: Mixed. Banks with strong commercial pipelines and mortgage exposures reacted to credit- and rate-sensitive headlines, while diversified financials tracked both equity market flows and deal-related announcements.

Technology: While the tech complex overall showed signs of continued valuation pressure in many mid- and small-cap names, the largest mega-cap names outperformed, as discussed below.

Key Economic Data and Fed Implications

There were no major surprise macro releases that reset the Fed narrative today, but sector-driven inflation dynamics — particularly the energy-led uptick — are likely to be monitored closely by fixed income traders and Fed watchers. A rise in energy costs can have two implications for policy expectations:

- Near-term upside risk to headline inflation, which could keep the Fed's bar for easing higher than previously expected, and

- Potentially divergent effects on real activity, where higher energy costs can act like a tax on consumption and weigh on cyclicals.

Market participants noted that the Fed's path remains data dependent. With mixed signals across the economy — softer manufacturing and small-cap weakness versus pockets of strength in energy and real estate — the central bank is likely to emphasize incoming CPI and payroll readings when shaping its near-term messaging. Any persistent move higher in commodity-driven inflation could delay market expectations for rate cuts and influence curve positioning.

Notable Individual Stock Moves

Megacaps (NVDA, AAPL, GOOGL, AMZN, MSFT): Institutional flows and a cluster of program trades that market sources pegged at roughly $16 billion in gross notional activity among the largest tech names were credited with propelling the Nasdaq-100. That activity helped lift QQQ even as broader tech valuations remain under pressure.

Energy names (XOM, CVX, BP): Broad sector strength was visible across integrateds and explorers. Commodity-price sensitivity and improved cash-flow narratives supported gains.

Real estate/REITs (select high-yield REITs): Transaction announcements and capital activity sparked outperformance in parts of the sector.

Industrials (BA, CAT, GE): These names were pressured by softer manufacturing indicators and profit-taking after recent rallies. Comments from PMs and supply-chain updates suggested demand recalibration.

Crypto-related equities (COIN, ETF issuers): Mixed. The Grayscale Ethereum Staking ETF 8-K filings and parallel disclosures attracted attention and created short-term trading in crypto-adjacent securities; price moves were uneven as regulatory and product-structural questions linger.

Small-cap and micro-cap gaps: Several small-cap stocks underperformed as liquidity rotated toward larger, more liquid megacaps and commodity-linked cyclicals.

Market commentary emphasized that today's winners and losers were as much a function of flows and positioning as they were fundamental updates.

Technical and Market Breadth Notes

Breadth remained narrow: QQQ leadership with SPY modestly positive and IWM negative suggests breadth metrics were unimpressive. Historically, rallies concentrated in mega-cap leadership without improving breadth can leave the market vulnerable to reversals if the leaders falter.

Volatility: Sector rotation tends to raise cross-sectional volatility even when headline indices move modestly. Traders should expect choppiness as positions are reallocated ahead of key macro releases.

Options activity: Increased notional around megacaps and energy names suggested options markets were pricing directional trades and hedges, consistent with institutional repositioning.

Outlook — What to Watch Next Session

Inflation and payroll signals: Any upcoming CPI/PCE or employment data will be central. Given the energy move today, even small upside surprises in inflation measures could recalibrate market expectations for Fed timing on rate cuts.

Earnings and deal flow: Continued M&A and financing updates in real estate and materials could sustain those rallies. Conversely, disappointing industrial or small-cap earnings would reinforce the current narrow leadership.

Leadership sustainability: Watch whether megacap tech can hold gains and whether leadership broadens beyond a handful of names. A widening advance would be constructive; continued narrowness would increase downside risk.

Energy and commodity trajectories: If the supply-tightness narrative extends, commodity-sensitive sectors could continue to outperform; that would have implications for inflation trajectories and policy expectations.

Market breadth and volume: Improvement in breadth and higher participation from small caps would signal healthier risk-on sentiment. If breadth deteriorates, traders may view the current moves as rotation-driven and vulnerable to reversal.

Historical Context

The current pattern — megacap-led rallies with selective sector rotation into commodity- and deal-driven names — is reminiscent of past episodes where liquidity and program flows determine short-term leadership while broader cyclical fundamentals take longer to re-accelerate. Historically, durable market advances require breadth expansion beyond the top handful of names; without that, upside tends to be capped and volatility higher.

Risk and Positioning Considerations (Informational Only)

Analysts note that markets remain sensitive to policy signals and macro surprises. Momentum currently favors larger, more liquid names and sectors with idiosyncratic narratives (energy, real estate, materials). Traders focusing on shorter time frames should monitor volatility and liquidity, while longer-term allocators are watching inflation trends and corporate earnings for confirmation of durable trends.

Investment Disclaimer

This report is for informational purposes only. It does not constitute investment advice, recommendations to buy or sell securities, or personalized financial guidance. Analysts and data referenced here reflect market observations and do not imply endorsements of specific securities or strategies.

Bottom Line

Today was a rotation day: QQQ outperformed as megacap activity lifted tech, while energy's supply-driven rally and deal activity in real estate and materials provided pockets of strength. Small caps and industrials lagged, leaving the overall picture mixed. The next session will be dominated by macro data and whether flows broaden beyond the day's narrow leadership. For now, markets remain selective, and the path forward will hinge on inflation signals, liquidity patterns and confirmation of earnings and deal-driven narratives.

Sources

+ 10 more sources

Use these insights — enter this week's contest.

Free practice contests — earn Alpha CoinsExplore More Content

Disclaimer: StockAlpha.ai content is for informational and educational purposes only. It is not personalized investment advice. Sentiment ratings and market analysis reflect data-driven observations, not buy, sell, or hold recommendations. Always consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.