Listen to this Recap

7:39

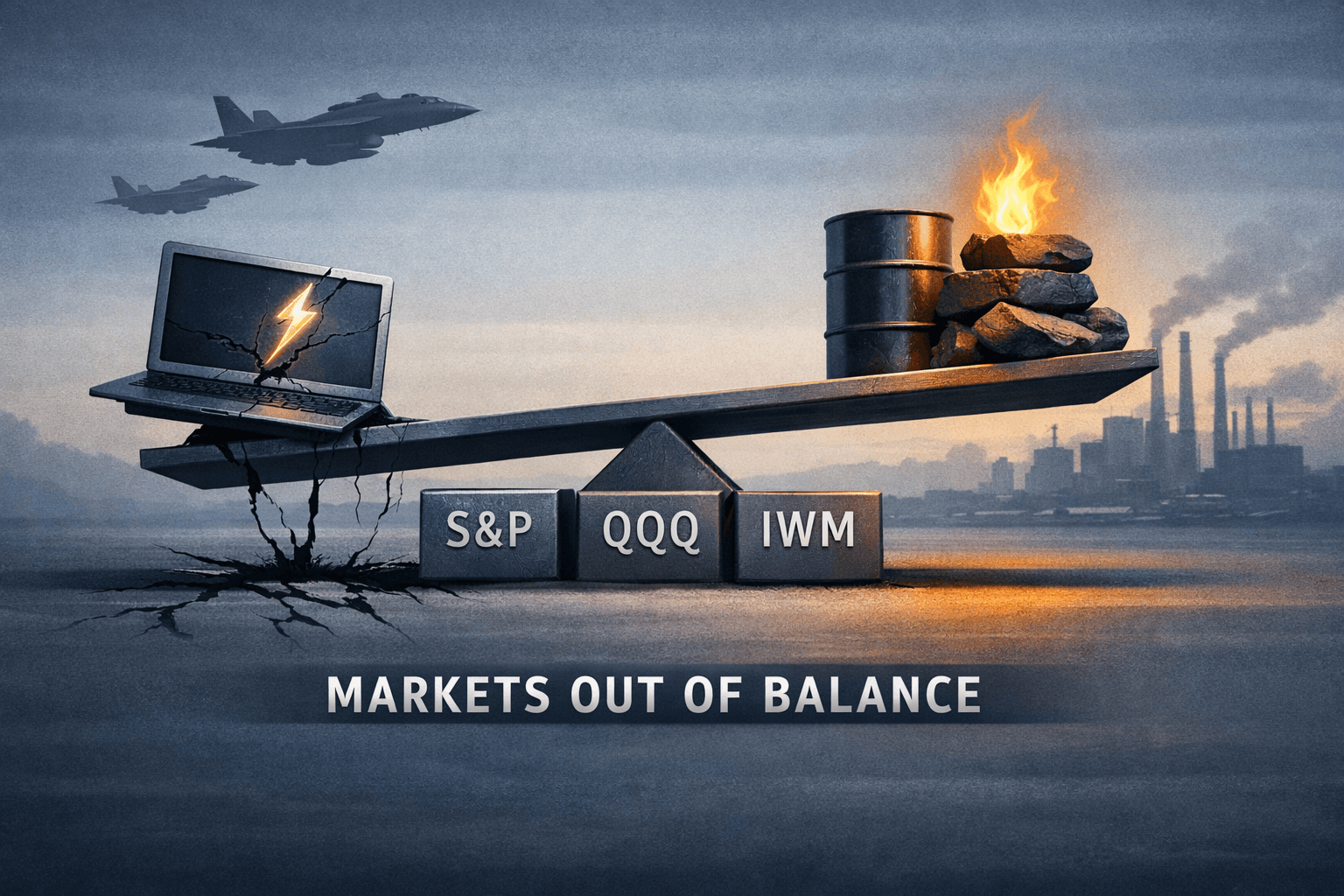

Tech Slips as Geopolitics and an Energy Supply Shock Reprice Risk; Stocks Finish Mixed

Podcast • Loading audio...

Share this article

Spread the word on social media

Key Takeaways

- •SPY down ~0.5%, QQQ down ~1.3%, IWM down ~0.8% — tech underperformed while energy and materials led.

- •Geopolitical headlines and an energy supply shock drove rotation from growth into commodity-linked sectors.

- •Crypto security incident added to intraday volatility for crypto-adjacent equities and fintech names.

- •Macro and Fed considerations remain paramount: higher energy prices could complicate the inflation picture.

- •Next session catalysts include geopolitical developments, oil/inventory data, and upcoming inflation/Fed commentary.

Today's market narrative — risk repriced, rotation reappears

Markets moved on a clear theme Tuesday: a spike in geopolitical risk and an energy supply shock prompted a classic rotation out of the biggest tech names and into commodity-linked sectors. The S&P 500 (SPY) closed down 0.5% while the tech-heavy Nasdaq-100 (QQQ) underperformed, sliding 1.3%. Small caps also gave back ground, with the Russell 2000 ETF (IWM) down about 0.8%.

That trio of moves — modest S&P weakness, sharper Nasdaq losses and small-cap lagging — captured the day's tug of war. Investors pared exposure to richly valued growth names sensitive to geopolitical headlines; money rotated into cyclical and commodity-exposed names that stand to benefit from higher energy prices and renewed resource demand.

Sector rotation and standout performers

Energy and materials led the winners. A reported supply shock in oil markets — amplified by headlines on disruptions and shifting inventory expectations — pushed crude prices higher and sent energy names sharply up relative to the broader market. Materials and mining stocks also showed momentum as exploration and deal activity lifted sentiment in the space.

Conversely, communication services and technology led the declines. Headlines that reportedly included threats targeting major chip- and consumer-tech companies weighed on the sector, with the Nasdaq-100 bearing the brunt of the selling. Utilities and defensive sectors were mixed: some utility subgroups gained on grid and nuclear policy developments, while renewable-linked names reacted to specific solar and permitting news.

Financials were in the middle of the pack. Banking and insurance names held up reasonably after a relatively quiet set of earnings and 8-K filings, while some broker-dealer and fintech names saw volatility tied to cryptocurrency developments discussed below.

Why the market moved — the drivers

Geopolitical headlines: Reports that Iran had made threats against major U.S. tech targets created an immediate risk-off impulse in the most rate-sensitive, high-valuation parts of the market. The reaction was concentrated in chipmakers and consumer-tech giants whose revenue or supply chains could be affected.

Energy supply shock: News that tightened oil supply expectations — a mix of outages, logistics disruptions and compressed inventories in certain regions — pushed oil prices higher. That's the principal reason energy stocks outperformed and why the broad market's defensive positioning was uneven.

Crypto and institutional flows: A security incident in the cryptocurrency space (the Drift hack) combined with ongoing institutional inflows/outflows created headline volatility for crypto-exposed equities and service providers. That added a supplementary source of risk sentiment and helped channel flows into traditional commodity and industrial names.

Macro and Fed backdrop: Even with no major surprise economic print today, the market is still pricing a relatively hawkish Fed path compared with a year ago. Traders are balancing the inflation persistence narrative with cautious optimism that growth isn't collapsing — a dynamic that tends to favor cyclical names when commodities spike and to penalize long-duration growth exposure.

Notable individual movers

Nvidia (NVDA) and Apple (AAPL): Both among the largest drags on the Nasdaq-100 after geo-politically tinged headlines. The shares underperformed as traders reassessed risk to supply chains and demand-sensitive narratives.

Major energy names (e.g., XOM, CVX, APA): Outperformed the market amid the oil-price move. Energy was the day’s clear sector winner, offsetting weakness elsewhere.

Materials/miners (e.g., FCX, NEM): Advanced after deal and exploration news that revived momentum in the mining complex.

Healthcare (e.g., Eli Lilly-equivalent discussion): Healthcare showed pockets of strength following regulatory approvals and positive company-specific developments, although policy noise kept the sector from being uniformly strong.

Select utilities and grid-related plays: Reacted to a flurry of news about grid upgrades, solar permitting and nuclear developments — the net effect was mixed but notable for investors watching infrastructure-related themes.

Note: ticker examples above are illustrative of sector moves and reflect broad market flow; they are not investment recommendations.

Economic data and Fed implications

There were no blockbuster macro prints today, but traders remain focused on a steady cadence of inflation and labor data due in the coming days and weeks. The market continues to price a higher-for-longer Fed profile than it did a year ago, which means that any fresh signs of sticky inflation or upside surprises in growth data can disproportionately shift risk premia.

Because energy prices ticked higher today, headline inflation trajectories — already under close watch — may receive a near-term lift. Analysts note that rising commodity prices complicate the Fed’s decision matrix: higher energy feeds into CPI readings and real-income dynamics, which could entrench a hawkish tone if sustained.

Fed speakers and upcoming monthly prints (PCE, CPI, jobs) will therefore be watched closely. In short, today's rotation should be viewed through the lens of a market that still judges policy to be a central risk — and whose reaction function is more volatile in the face of commodity and geopolitical shocks.

Technical and breadth read

Technically, the pattern was a sector-led divergence: breadth tightened as leadership narrowed to energy and materials while growth leadership at the top of the market weakened. That dynamic often precedes periods of either consolidation or a wider risk-off leg if the headlines persist.

From a practical standpoint, traders will look at whether the S&P can hold recent support levels and whether the Nasdaq can re-establish near-term technical footholds. Continued underperformance by QQQ relative to SPY would signal that money is still rotating out of growth into cyclicals — a configuration that can produce higher volatility even if the headline indices don’t move dramatically.

Crypto wrap — Drift hack and institutional flows

A security incident in the Drift protocol and ongoing institutional allocation decisions added to risk-on/risk-off swings in crypto-linked equities and service providers. Exchanges and custody providers saw intraday repricing after the hack, and several fintech names with crypto exposure underperformed. The episode reminded markets that operational and security risks remain material for the crypto ecosystem, and that spillovers to listed equities are possible.

Earnings, filings and corporate news

A number of 8-K filings and corporate updates crossed the tape today (Atlas Energy Solutions, Target Hospitality, Bioxcel Therapeutics, Profound Medical, and others). While most were company-specific and did not move the entire market, they contributed to sector-level narratives — energy and healthcare names were the primary beneficiaries of positive technical or operational disclosures.

Retail and consumer names showed a mixed reaction to earnings and search trends (Nike-related buzz was notable in retail search data). Analysts flagged that high-frequency consumer data still shows pockets of resilience even as spending patterns remain uneven.

What this means for investors and traders

Rotation is active: The move today is consistent with a rotation into cyclical/commodity sectors when geopolitical risk intersects with supply-side commodity moves. Traders note that such rotations can persist for several sessions if fundamentals or headlines reinforce them.

Volatility remains headline-sensitive: The market’s sensitivity to geopolitical and operational headlines suggests an elevated probability of intraday swings. Position sizing and risk management remain important as sector leadership can flip quickly.

Macro calendar matters: With inflation data and Fed remarks still on the calendar, any durable shift in commodity prices could affect the policy outlook and therefore market leadership.

Investment disclaimer: This commentary is for informational purposes only and does not constitute investment advice. It is not a recommendation to buy, sell, or hold any security. Analysts and market data referenced reflect observations and consensus views, not personalized financial counsel.

Outlook — what to watch next session

Geopolitical headlines: Any clarification, escalation or de-escalation around the reported threats will likely move tech and defense-linked names. Traders should expect headlines to drive short-term flows.

Energy data: Inventory reports and any additional supply developments will be the proximate driver for energy and materials; sustained higher oil would keep cyclical leadership intact and could complicate the Fed inflation outlook.

Macro prints and Fed speak: Upcoming inflation and labor data remain the multi-day market backdrop. Even absent shocks, the market is primed to react to small surprises.

Crypto security fallout: Any follow-on from the Drift incident — whether reimbursement, regulatory attention, or contagion — could continue to pressure crypto-adjacent equities.

Technical confirmation: Watch whether SPY can re-center above recent short-term moving averages and whether QQQ stabilizes; persistent Nasdaq underperformance would reinforce the bearish tilt for growth sectors.

Bottom line

Tuesday’s tape was dominated by a rotation driven by geopolitical headlines and an energy supply shock. The S&P 500 (SPY) ended the day down about 0.5%, the Nasdaq-100 (QQQ) fell roughly 1.3%, and small caps (IWM) declined approximately 0.8%. The moves underscore a market environment where headlines matter, commodity price action can shift leadership quickly, and the Fed/ inflation story remains the overarching policy backdrop. Analysts say a period of higher intraday volatility is likely until either the geopolitical situation or commodity pressures clearly resolve.

Key catalysts to monitor for tomorrow: geopolitical updates, oil/inventory data, and any Fed-related comments or inflation leads. As always, traders are advised to weigh technical setups against fundamental developments and to manage risk accordingly. This report is informational and should not be construed as financial advice.

Sources

+ 10 more sources

Use these insights — enter this week's contest.

Free practice contests — earn Alpha CoinsExplore More Content

Disclaimer: StockAlpha.ai content is for informational and educational purposes only. It is not personalized investment advice. Sentiment ratings and market analysis reflect data-driven observations, not buy, sell, or hold recommendations. Always consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.