Listen to this Recap

8:15

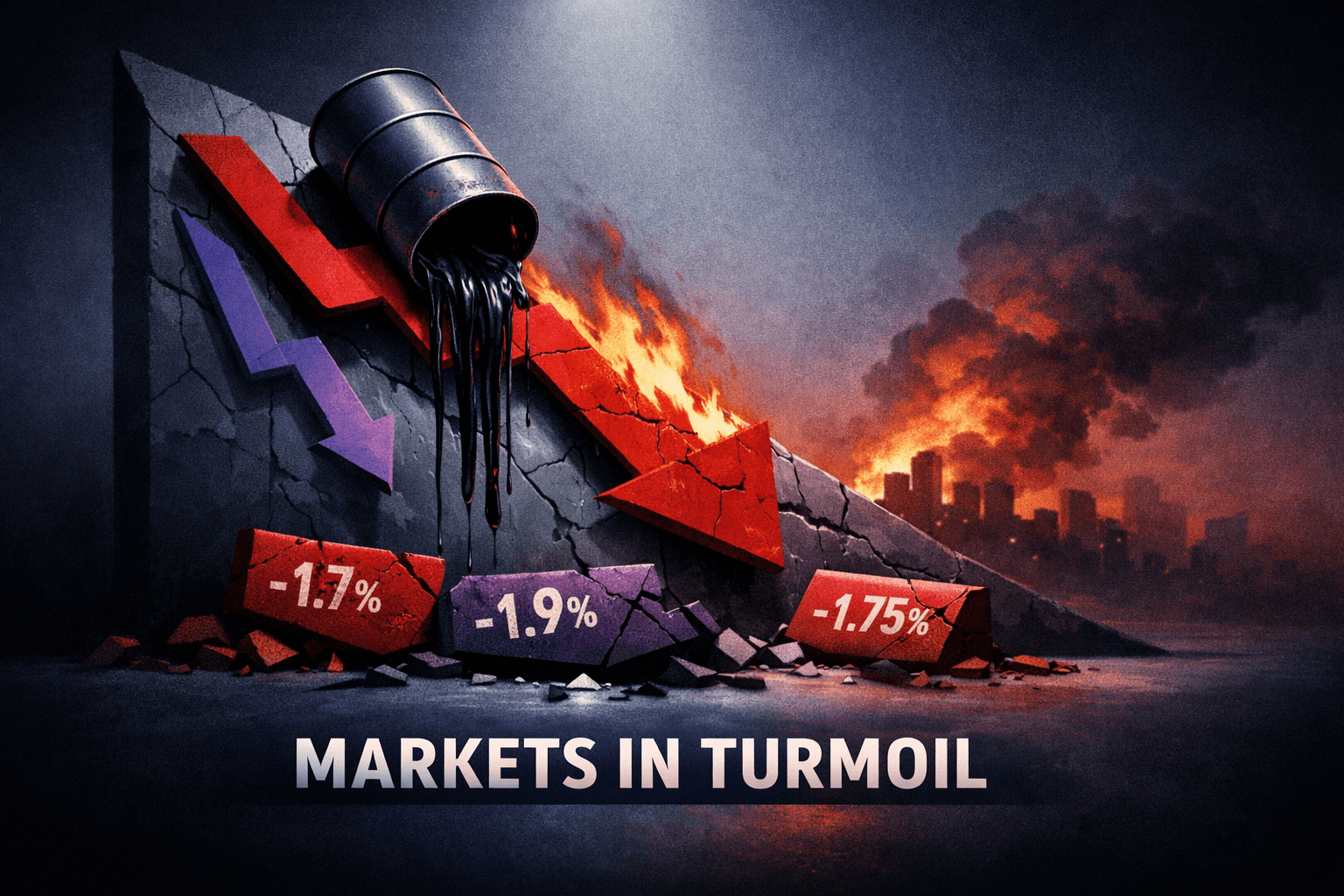

Markets Slide on Oil Shock and Risk-Off Sentiment; Tech and Small Caps Lead Declines

Podcast • Loading audio...

Share this article

Spread the word on social media

Key Takeaways

- •Broad sell-off: SPY -1.71%, QQQ -1.95%, IWM -1.75% — tech and small caps led losses.

- •Oil spike from an Iran-related development amplified inflation and Fed policy uncertainty.

- •Sector split: energy and select communications/media outperformed; tech, financials and crypto-related names lagged.

- •Company-specific catalysts (e.g., AstraZeneca trial win) can still drive idiosyncratic moves amid macro-driven sessions.

- •Near-term outlook is data-dependent: watch oil, Fed commentary, inflation prints and earnings.

Market narrative: geopolitics and policy jitters push markets lower

The S&P 500 (SPY) closed down 1.71% while the tech-heavy Nasdaq-100 (QQQ) tumbled 1.95%. Small-cap stocks, tracked by the Russell 2000 ETF (IWM), also struggled, finishing the session down 1.75%. Those index moves set the tone for a broad risk-off day, where rising oil prices, renewed geopolitical tensions and signs of policy friction combined to sap investor appetite for cyclical and growth exposures.

Short-term market action was decisive: equities weakened across the board as oil surged on an Iran-related supply risk, futures opened lower and rotation out of higher-beta names picked up pace. The depth of the decline in QQQ outpaced the S&P, signaling that technology and other growth sectors bore a larger share of the selling pressure. At the same time, IWM’s roughly similar decline to SPY suggests breadth deterioration extended into smaller-cap, domestically oriented names.

Why markets moved: oil shock, geopolitical headlines, and policy uncertainty

Several visible catalysts converged today. The most immediate was a jump in crude prices after reports of an Iran-linked development that market participants read as a heightened supply risk. Energy-sensitive parts of the market reacted quickly: oil-related names and commodity-linked sectors retraced earlier weakness and, in some cases, rallied intraday. That spike in energy costs reverberated through broader sentiment — higher oil raises the risk of renewed inflationary pressure and complicates the Federal Reserve’s policy calculus.

Compounding the commodity shock were reports of renewed selling in the crypto complex and elevated policy pressure on financials. Headlines that flagged stronger regulatory scrutiny around crypto and softening demand signals in some cyclical pockets helped accelerate the risk-off move. Together, these forces shifted positioning away from rate-sensitive and long-duration assets, notably large-cap tech stocks that dominate QQQ.

Sector rotation and standout performers

The day’s sector map was a clear narrative of winners and losers driven by headlines and macro signals:

Energy: With oil moving notably higher, energy stocks showed relative strength. The sector benefited from a near-term supply scare, and names with direct exposure to crude and services outperformed intraday. The energy-led upside was not large enough to offset losses elsewhere, but it was a clear defensive haven for part of the session.

Communications & Media: The communications/media complex showed pockets of momentum, as headline-driven flows and select corporate news helped certain content and ad-revenue-exposed names hold up better than broader tech. M&A chatter and re-rating for advertising recovery also supported the group.

Utilities: Utilities wrapped the session mixed-to-weak as rising rates and risk aversion weighed on the long-duration, dividend-sensitive group. Despite the defensive characteristics of the sector, the upward pressure on oil and policy uncertainty made pure safety plays less of a focal point.

Materials & Mining: Materials were mixed, with miners reacting to both the crude move and ongoing commodity demand headlines. Deal flow in real assets and a cautious view on global growth skewed sentiment toward select quality miners.

Real Estate: Real estate activity picked up on deal flow headlines, but the group still felt pressure from the broader rates and risk-off narrative. Investors watched how higher energy costs and policy uncertainty could affect operating fundamentals for property owners.

Industrials & Manufacturing: The industrials complex was pressured by the risk-off tone and supply-chain concerns tied to geopolitical developments. Stocks tied to discretionary capex and trade-sensitive exposure underperformed.

Consumer & Retail: Consumer and retail names were mixed but generally weaker as the sell-off in small caps and discretionary faded into the afternoon. Analysts flagged that rising oil is an indirect tax on consumer wallets and could temper spending momentum.

Financials: Banks and finance-related stocks felt policy headwinds. With Fed path ambiguity amplified by inflationary signals from energy, financials traded under pressure as investors weighed margin dynamics and credit sensitivity in a higher-rate, slower-growth scenario.

Crypto-related equities: The crypto sector saw selling pressure on renewed regulatory policy headlines, and blockchain/mining names underperformed relative to broader market averages.

Notable individual movers

AstraZeneca (AZN) jumped roughly 4% after a surprise clinical trial win, according to headlines. The biotech’s trial surprise was one of the clearest single-stock positive catalysts on the day, and the move provided a reminder that company-specific news can still create strong directional trades even in risk-off sessions.

O'Reilly Automotive (ORLY) drew attention after an analyst note titled "3 Reasons We Love This Stock." Coverage and positive sentiment around O'Reilly helped support its shares relative to the retail auto aftermarket complex.

Energy names rallied on the oil move; several large energy producers and service providers outpaced the broader market as short-term flows chased commodity exposure.

Several smaller names filed 8-Ks (Two Harbors Investment Corp., Bioxcel Therapeutics, PMGC Holdings, Reliance Global Group, National Cinemedia), drawing episodic interest but not enough to alter the broader market direction.

Crypto exchanges and miners were among the session’s laggards after headlines signaled renewed policy pressure; names tied to digital-asset trading and mining underperformed as the risk-off dynamic accelerated.

Technical and breadth signals

Technically, the market’s internals showed a clear deterioration. QQQ’s greater drop relative to SPY is an important signal: large-cap growth leadership wavered, and that often precedes broader risk repricing. Declining breadth, coupled with weakness across small caps (IWM -1.75%), suggests that liquidity-sensitive, domestically exposed companies were not immune to the day’s pressure.

From a volatility perspective, the VIX and sector-specific volatility measures rose as investors sought optionality to hedge against further downside surprises. Momentum indicators flipped in key large-cap names, and traders noted heavier volume on the sell side — a classic sign of distribution when combined with macro catalysts.

Fed implications and economic framing

While no new, definitive Fed action was announced today, the market’s reaction crystallized a few policy implications:

Higher oil raises the risk of sticky inflation at the margin. If oil remains elevated, it complicates the picture for the Fed by increasing the likelihood that headline inflation prints stay above comfort levels, which could delay easing expectations or even force a reassessment if upside surprises persist.

Policy uncertainty is now a two-way risk: persistent inflation from energy versus growth slowing from higher real costs. Markets are therefore pricing a wider distribution of Fed outcomes, and that feeds into greater volatility and sector repricing.

Banking and financial sectors continue to be sensitive to the short end of the curve and to forward-rate expectations. With Fed path ambiguity, balance-sheet and funding dynamics remain a watch point for analysts.

Analysts note that the current price action is consistent with a market that is repricing both growth and inflation risks simultaneously. That complexity typically favors shorter-term tactical positioning over long-duration bets until clearer macro signals re-emerge.

Historical context

This kind of session — where oil spikes on geopolitical news and growth names lead the decline — is not unprecedented. Historically, similar days have produced short-term volatility spikes and prompted rotation into energy, defensive sectors and selected value names. The difference this time is the concentrated exposure of market-cap-weighted indices to a handful of mega-cap tech names, which amplifies the headline index moves when growth stocks underperform.

What to watch next

Heading into the next session, market participants said they will be watching a few specific datapoints and catalysts:

Oil price trajectory: Whether the crude move is a transient headline-driven spike or the start of a more sustained re-pricing. A second consecutive day of rising oil would increase inflationary concerns and extend the risk-off mood.

Fed speakers and minutes: Any comments that clarify the Fed’s tolerance for higher inflation or the timing of policy adjustments will be closely parsed. The market is particularly sensitive to language that hints at a longer-than-expected period of restrictive policy.

Economic releases: Data points that speak to inflation, wage growth and consumer resilience (e.g., CPI/ PCE readings, employment measures, consumer confidence) will be market-moving if they deviate from expectations.

Earnings and company-specific catalysts: Company news such as the AstraZeneca trial surprise underscores how corporate announcements can create idiosyncratic winners even in down markets. Upcoming earnings reports and guidance will be tested against the day’s risk-off backdrop.

Crypto and regulatory headlines: Additional policy or enforcement announcements could prolong pressure in crypto-related equities and the exchange complex.

Outlook: cautious and data-dependent

Today’s price action argues for a cautious near-term stance among market participants. The combination of an oil-driven inflation scare, geopolitical uncertainty and policy ambiguity has pushed volatility higher and prompted a re-evaluation of exposure to long-duration and small-cap names. Analysts say that until the market gets clearer confirmation on whether the oil move is sustained and how the Fed will react materially to any inflation surprise, investors are likely to favor defensive positioning and shorter-duration exposures.

That said, markets often overshoot on headline-driven moves. If oil cools and risk sentiment normalizes, oversold technology and growth names could see quick snapbacks. Conversely, if geopolitical tensions escalate or inflation data accelerates, the path for rates and equities could tilt further toward downside.

Final takeaways

- The S&P 500 (SPY) fell 1.71%, the Nasdaq-100 (QQQ) dropped 1.95%, and the Russell 2000 (IWM) declined 1.75% — a broad risk-off day with tech and small caps leading.

- Oil’s jump on an Iran-linked move was the proximate catalyst, lifting energy but weighing on the inflation outlook and complicating the Fed’s policy path.

- Sector rotation favored energy and select communications/media names while tech, small caps, financials and crypto-related equities lagged.

- Company-specific news still created standout moves (AstraZeneca’s trial win), but macro headlines dominated the tape.

- Near-term risk remains elevated: watch oil, Fed commentary, inflation prints and corporate news to gauge whether today’s repricing extends or reverses.

Investment disclaimer: This recap is for informational purposes only. It is not a recommendation to buy, sell or hold any security. Analysts note market dynamics and risks but do not offer personalized investment advice.

Sources

+ 10 more sources

Use these insights — enter this week's contest.

Free practice contests — earn Alpha CoinsExplore More Content

Disclaimer: StockAlpha.ai content is for informational and educational purposes only. It is not personalized investment advice. Sentiment ratings and market analysis reflect data-driven observations, not buy, sell, or hold recommendations. Always consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.