Listen to this Recap

7:52

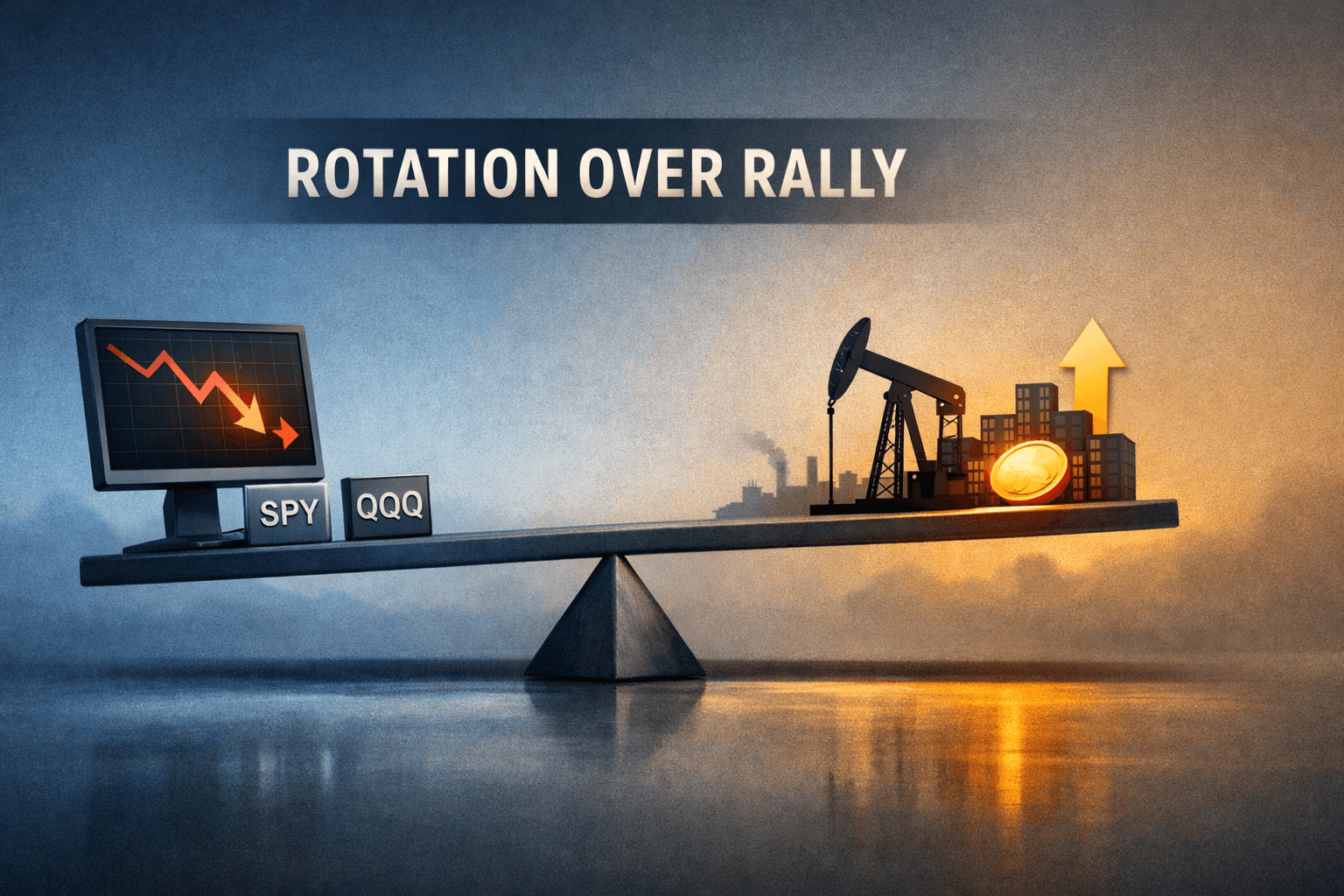

Rotation Over Rally: Energy and Small Caps Outperform as Tech Pauses — SPY and QQQ Slip

Podcast • Loading audio...

Share this article

Spread the word on social media

Key Takeaways

- •SPY and QQQ finished slightly lower (SPY -0.25%, QQQ -0.32%) while small caps outperformed (IWM +0.65%), signaling a rotation into cyclical and commodity-linked names.

- •Energy led the tape as oil neared $110, boosting energy and materials stocks and complicating the Fed’s path toward rate cuts.

- •Cannabis policy momentum, optical/ materials re-rating, and crypto institutionalization created sector-specific catalysts that drove selective strength.

- •Fed hopes for future rate cuts remain priced in by markets, but higher commodity prices and geopolitical risks make outcomes conditional.

- •Watch oil, Fed commentary, and breadth metrics next session to determine whether today’s rotation broadens into sustained leadership change.

Market snapshot and the day's narrative

The S&P 500 (SPY) closed down 0.25% while the tech-heavy Nasdaq-100 (QQQ) slipped 0.32%. In a notable divergence, small-cap stocks outperformed, with the Russell 2000 ETF (IWM) up 0.65%. That split — large-cap tech giving back a little ground while smaller, more cyclical names and energy names rallied — defined the market's behavior on March 19.

Broadly, the day felt like a rotation session rather than a market-wide selloff. Investors appeared to redeploy gains from mega-cap technology into energy, materials, and certain domestic cyclical plays. The backdrop driving that reweighting: oil pushing toward the $110/barrel area, fresh momentum in commodities and materials, and ongoing policy developments around niche but market-moving themes such as cannabis uplisting and institutional crypto interest.

Why the tape looked mixed: forces at work

Several cross-currents explain the divergence between the major cap-weighted indices and smaller-cap, commodity-linked groups.

- Commodity-driven leadership: Energy strengthened as oil neared $110, which lifted energy stocks and related sectors. A stronger oil price supports energy profitability, and the market rewarded names exposed to higher commodity realizations.

- Rotation from growth to cyclical/small-cap exposure: With long-duration growth names mildly under pressure, funds appear to be rebalancing into cyclicals and domestically oriented small caps that stand to benefit from stronger commodity and real-activity indicators.

- Fed policy calculus remains fluid: Rate-cut hopes remain alive in sentiment channels, but higher oil and firmer commodity momentum complicate the path to easier policy by keeping upside pressure on inflation expectations. Markets are thus simultaneously pricing in eventual easing while re-pricing near-term risk from commodity-driven inflation.

- Sector-specific newsflow: Policy tailwinds in cannabis, optical and materials sector re-rating, and industry-specific 8-K filings and upgrades created pockets of rotation beyond the index headlines.

Index and breadth implications

The day’s action — SPY and QQQ slightly negative while IWM climbed — signals uneven breadth. When small caps outperform while the large-cap leadership softens, it often reflects a confidence in domestic cyclical activity or a tactical portfolio rebalancing away from the most richly valued large-cap tech names.

Historically, similar divergences have preceded periods where market leadership broadened (if macro conditions improved) or where small caps ran ahead briefly before mean-reverting. Today’s pattern suggests market participants are looking for alternative drivers of returns beyond the mega-cap growth cohort.

Sector rotation and standout performers

Sector movement favored commodity- and domestic-oriented groups.

- Energy: The clear standout. With oil trading near $110, energy shares and ETFs outperformed. Strength here was broad-based — integrated producers, services, and refiners all showed positive price action as traders priced stronger margins and revenue outlooks.

- Materials & Mining: Momentum built in materials names, consistent with stronger commodity prices and the OFC conference confirming an optical supercycle that has repriced parts of the semiconductor-capital-equipment and materials supply chain.

- Real Estate: Select REITs showed momentum tied to leasing and sales activity. The real estate space appears to be discriminating — assets with strong leasing demand and repricing potential received more attention.

- Utilities & Communications: Utilities and communications saw mixed returns as investors weighed defensive positioning against higher input-cost risk. Communications and media moved on network upgrade and ratings news, producing selective gains and losses depending on the company story.

- Technology: Tech weakness was concentrated in the largest cap growth names that populate QQQ. AI and logistics momentum headlines supported pockets of strength in software and retail-related tech, but they weren’t enough to offset weakness in some mega-cap names.

Key economic and Fed implications

There was no blockbuster macro print today, but the policy narrative remained central.

- Rate-cut hopes: Market commentary continues to suggest investors are hoping for rate cuts later this year — that narrative persists. However, the prospect of sustained higher oil and commodity prices complicates the Fed’s path because higher energy costs can translate into stickier inflation readings.

- Fed watch: Analysts note that while the Fed’s longer-run stance may still allow for easing if growth cools, any near-term uptick in inflation or inflation expectations will likely keep the Fed on a cautious footing. The interplay between commodity-driven inflation signals and labor-market resiliency will be pivotal in shaping expectations.

- Geopolitical risk premium: JPMorgan’s note that investors may be complacent over Iran-related conflict risk is an important reminder that geopolitical shocks could inject volatility into energy markets and broader risk assets.

In short, the Fed picture remains one of conditional easing — markets want cuts but higher oil and commodity momentum make that conditionality less certain.

Notable individual-stock and sector-specific moves

Today’s tape featured several thematic and company-specific developments that caught traders’ attention:

- Cannabis sector: Momentum on cannabis policy and talk of uplisting and legislative moves (including discussions around H.R. 7987) sparked interest across U.S.-listed cannabis names. The potential for an uplisting or federal policy changes remains a thematic catalyst that could reprice the sector if enacted.

- Optical and materials names: OFC 2026 confirmations around an optical supercycle and demonstrations like Poet’s Starlight Gen 2 injections into optics narratives helped lift suppliers and materials firms tied to fiber and optical-capacity upgrades.

- Large industrials & machinery: Titan Machinery and other industrial filings drew attention in the manufacturing and equipment space; trade and robotics themes pulled forward re-rate conversations for industrial automation players.

- Biotech and small-cap filings: Several 8-K filings (Humacyte, Micro Imaging Technology, Acrivon Therapeutics) produced idiosyncratic moves in the small-cap and micro-cap biotech space. These remain story-driven and volume-sensitive.

- Crypto-related plays: Institutional cryptocurrency momentum pushed interest in miners, exchange-related stocks, and fintechs with crypto exposure. The newsfeed indicated accelerating institutional activity into crypto, which can lift a narrow set of equities even when broader markets are mixed.

Technical & positioning notes traders should watch

While we won’t offer trading advice, market technicians and active traders will likely watch the following:

- The divergence between cap-weighted indices (SPY/QQQ) and IWM: sustained small-cap outperformance would be a notable shift in leadership.

- Oil breakouts: A continued push above $110 for Brent/WTI is both a macro and market risk factor for inflation expectations and sector rotation.

- Breadth indicators: Whether the stock-specific strength broadens beyond energy and materials into industrials and services will be important to judge the sustainability of the current rotation.

Outlook — what to watch for next session

Heading into the next trading day, several items are likely to set the tape’s tone:

- Oil and commodity prices: Any follow-through in crude above $110 could prolong the rotation toward energy and materials and complicate Fed rate-cut expectations.

- Fed speakers and economic calendar: Investors will continue to parse Fed commentary and any inflation or employment data that could confirm or disprove the market’s rate-cut optimism. Absent clear disinflation signals, the Fed is likely to maintain a cautious posture.

- Sector-specific catalysts: Developments in cannabis policy, OFC 2026 takeaways, and any company-specific filings (8-Ks among small-caps) can generate outsized moves in niche pockets.

- Geopolitical headlines: Any escalation in Middle East-related tensions would likely amplify energy-related moves and create risk-off dynamics in broader markets.

Taken together, the near-term outlook looks like a continuation of selective leadership rather than a broad, consensus-driven rally. Market participants will be watching whether today’s rotation into small caps and energy broadens into a sustained leadership change or proves to be a shorter-duration reallocation.

Bottom line

March 19 was a day of rotation: modest declines for the major cap-weighted indices (SPY down 0.25%, QQQ down 0.32%) contrasted with a small-cap bid (IWM up 0.65%). Commodity strength — most visibly in oil approaching $110 — and sector-specific catalysts (cannabis policy momentum, optical/ materials re-rating, and crypto institutionalization) drove a rebalancing of market leadership. The Fed remains the macro headline in the background: markets hope for cuts, but higher commodity prices make that path conditional and uncertain.

Investment disclaimer: This report is for informational purposes only. It does not constitute investment advice or a recommendation to buy, sell, or hold any security. Analysts note market risks and provide commentary on observable market dynamics; it is not personalized financial advice.

Sources

+ 10 more sources

Use these insights — enter this week's contest.

Free practice contests — earn Alpha CoinsExplore More Content

Disclaimer: StockAlpha.ai content is for informational and educational purposes only. It is not personalized investment advice. Sentiment ratings and market analysis reflect data-driven observations, not buy, sell, or hold recommendations. Always consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.