Listen to this Recap

8:27

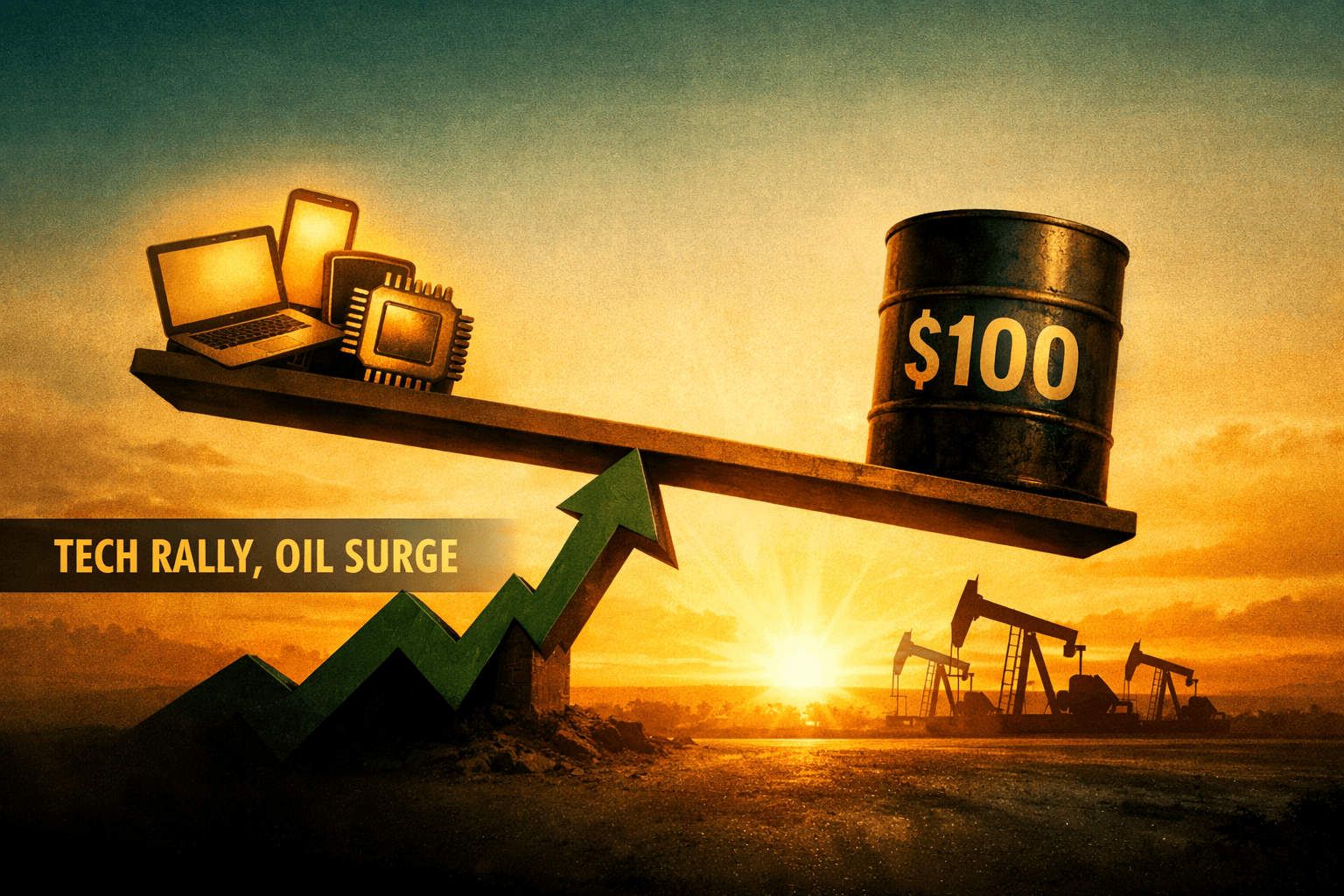

Risk-On Resume: Tech-Led Rally Lifts Benchmarks as Oil Holds Above $100

Podcast • Loading audio...

Share this article

Spread the word on social media

Key Takeaways

- •SPY +1.02% and QQQ +1.12% led a broad risk-on session; IWM also climbed 0.94%, signaling participation across market caps.

- •Tech leadership was reinforced by AI supply-chain news (POET/LITEON) and big-tech activity in carbon-credit markets (Microsoft noted), while energy’s hold above $100 supported cyclicals.

- •Macro crosscurrents — notably sustained oil strength — keep upside inflation risks on the table and make upcoming data/Fed commentary crucial.

- •Corporate and sector headlines (Airbus deliveries, MoCaFi bankruptcy, multiple 8-K filings) drove idiosyncratic moves that will matter for sector rotation.

- •Near-term outlook: cautiously bullish if breadth continues to improve; watch oil, fixed-income pricing, ETF flows and next economic prints for confirmation.

Market snapshot — risk-on tone returns

The S&P 500 (SPY) closed up 1.02% while the tech-heavy Nasdaq-100 (QQQ) rose 1.12%. Small caps participated, with the Russell 2000 (IWM) climbing 0.94%, signaling a broad-based pickup in risk appetite across market caps.

Stocks opened the week with a clear risk-on tilt: large-cap growth led but breadth was constructive enough to lift small- and mid-cap indexes. The rally arrived amid a mix of sector-specific headlines — from big tech carbon-credit activity to a new POET Technologies/LITEON partnership for AI optical modules — and macro crosscurrents including Brent crude still holding above $100 per barrel.

The narrative: why markets moved

Several factors converged to produce today’s advance. First, momentum in big-cap tech names continued after recent strength, helping QQQ outpace SPY. Second, flows into crypto-related products appeared to feed a broader risk-on mood across markets: commentators flagged fresh ETF flows into crypto vehicles that coincided with gains in crypto-linked equities. Third, energy’s firmness (Brent above $100) underpinned cyclicals and commodity-sensitive names, helping support the S&P and small-cap performance.

At the same time, defensive sectors showed mixed signals: utilities registered pockets of strength tied to project wins, yet real estate headlines around deals and redevelopment plans kept that group under watch for idiosyncratic headwinds. Overall, the tape suggested investors were willing to rotate back into growth and cyclicals after a period of consolidation.

Sector rotation and standout performers

Technology/Communications: Tech and comms led the tape, consistent with QQQ’s 1.12% rise. Big tech’s activity around carbon-credit markets — Microsoft flagged as a leader in volume — was an unusual but constructive narrative that helped push software, cloud and select hardware names higher. Headlines about AI supply-chain upgrades (see POET/LITEON) also underpinned semiconductor- and optical-equipment-related names.

Energy: Oil staying north of $100 supported energy names and capital-goods suppliers tied to energy projects. The price backdrop raises both earnings upside for energy producers and cost/headline-risk for certain industrial and consumer sectors — a two-edged sword for the market.

Industrials & Materials: Industrial names were mixed but generally positive as Airbus reported 75 deliveries in Q1 (Barclays note), suggesting ongoing demand for durable goods. Materials and mining had pockets of strength tied to commodity momentum and project wins.

Financials: Finance and banking moves were tied to idiosyncratic headlines — including the MoCaFi bankruptcy and related court developments — which pressured some regional and fintech-linked names even as broader financials held up on the day.

Real Estate & Utilities: Real estate faced headwinds from redevelopment news and sector-specific deal dynamics, while utilities showed selective momentum where project wins improved the outlook for growth and cash flow stability.

Crypto-related equities: A rebound driven by ETF flows helped lift listed crypto and blockchain-related names; the move supported risk-on sentiment across the market.

Macro and Fed implications

There were no big macro prints today, but two crosscurrents are central to the Fed- and inflation-facing narrative investors are parsing:

Oil > $100: Sustained strength in Brent keeps upside risks to inflation on the table. Market participants will read persistent energy strength as a potential headwind to downbeat inflation prints, which could influence the Fed’s timing and messaging around rate easing. Analysts note that a prolonged period of elevated energy prices complicates the disinflation story and can compress real consumer demand in the quarters ahead.

Risk appetite & flows: Renewed risk-taking — visible in tech and crypto flows today — suggests market participants are comfortable with the current policy outlook for now. That said, the connection between equity rallies and fixed-income pricing will be key to the next leg: if Treasury yields climb meaningfully on inflation or growth repricing, the rally could meet resistance.

Taken together, the tape suggests investors currently price a path in which the Fed remains data-dependent, with elevated oil a watch item that could keep policy on guard. Economists and market strategists will be watching incoming CPI/PCE prints and employment data for confirmation that disinflation remains on track.

Notable individual moves and corporate headlines

POET Technologies / LITEON: The announced joint development of optical modules for AI applications put a spotlight on companies in the AI supply chain. Analysts note that partnerships like this can accelerate product road maps and potentially expand TAM for specialized optical components — positive sentiment for suppliers and equipment makers.

Microsoft: Reported to be a leading buyer in a surge of corporate carbon-credit activity; big-tech involvement in environmental markets is drawing investor attention and has been a source of outperformance for select green-technology and software suppliers.

ServisFirst Bancshares (SFBS): Featured in sector commentary today amid analyst coverage; banking-themed headlines including regional performance and credit considerations have kept the name under analyst scrutiny.

Electronic Arts (EA): Subject of a ‘buy/sell/hold’ discussion in coverage today; gaming and consumer software names are being re-evaluated as spending patterns and subscription monetization models evolve.

Airbus: Barclays flagged 75 aircraft deliveries in Q1, a constructive read on commercial aviation demand that benefits suppliers and industrials tied to air travel.

MoCaFi: The firm’s bankruptcy and associated court developments cast a shadow over some fintech-adjacent names and raised questions about credit and operational risk in the sector.

Corporate filings and smaller-cap 8-Ks: Opal Fuels, Addentax Group and Zenas Biopharma filed 8-Ks today; while these did not move the macro, they are examples of background corporate housekeeping and event-driven moves that can affect individual names.

Technical backdrop and breadth

The fact that SPY, QQQ and IWM all finished the day higher — with QQQ slightly outpacing SPY and IWM posting a near-parity gain — suggests the move was not narrowly concentrated. That said, leadership skewed toward growth/tech, and investors should watch whether breadth improves over the next sessions (new highs vs new lows, advancing volume vs declining volume) to confirm a sustainable uptrend.

Volatility measures remain relevant: a sustained drop in implied volatility alongside rising prices would reinforce a bullish reading, while a divergence (rising VIX on price gains) would warn of underlying fragility. With oil and supply-chain news in the background, rotational flows could accelerate sector-by-sector.

Historical context

Market participants often see periods like this — tech-led gains with energy support — in the late-cycle or sticky-inflation phases of market regimes. Historically, rallies that are accompanied by higher commodity prices can produce a two-step pattern: an initial advance followed by a chop as investors digest earnings and inflation prints. This underscores why the market will be sensitive to near-term economic releases and corporate guidance over the coming weeks.

What to watch tomorrow

- Energy headlines and oil prices: Any further move above $100 or a sharp pullback will have outsized implications for cyclicals, consumer names and inflation expectations.

- Fed commentary and economic data: Even in the absence of a Fed meeting this week, Fed speakers and upcoming CPI/PCE prints will be parsed for any indications of a shift in the timing of policy easing.

- Earnings and corporate developments: Watch for company-level announcements — particularly in tech, industrials and energy — that could either reinforce or challenge today’s sector rotation.

- ETF flows and crypto-related activity: Continued inflows into crypto ETFs would likely sustain risk appetite among certain equities; conversely, outflows could reverse some of the day’s gains.

Bottom line and near-term outlook

Today’s session was constructive: the S&P 500 (SPY) +1.02%, Nasdaq-100 (QQQ) +1.12% and Russell 2000 (IWM) +0.94% indicate a broad-based pick-up in risk-taking, with tech leadership and energy strength the principal drivers. Momentum suggests a cautiously bullish near-term outlook, but the persistence of high oil prices and upcoming macro prints mean the path forward is not without risk.

Traders and investors should monitor breadth, fixed-income reactions to commodity-driven inflation risks and upcoming corporate catalysts to gauge whether this rally has legs. Analysts note that confirmation would require improving breadth, steady or falling bond yields, and clean earnings beats or constructive guidance from major tech and industrial names.

Investment disclaimer

This note is for informational purposes only and does not constitute investment advice or a recommendation to buy, sell, or hold any security. Analysts’ views presented here reflect market analysis and are not personalized investment recommendations.

Sources

+ 10 more sources

Use these insights — enter this week's contest.

Free practice contests — earn Alpha CoinsExplore More Content

Disclaimer: StockAlpha.ai content is for informational and educational purposes only. It is not personalized investment advice. Sentiment ratings and market analysis reflect data-driven observations, not buy, sell, or hold recommendations. Always consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.