- Bid-ask spread is the difference between the price buyers will pay and sellers will accept; it represents an immediate trading cost you pay when using market orders.

- Spreads are smallest in highly liquid large-cap stocks and can be large in thinly traded or off-hours markets, sometimes costing several percent of your trade value.

- Using limit orders, trading during regular market hours, and choosing liquid securities help you reduce spread costs.

- Changes in the spread can signal shifting market sentiment, rising uncertainty, or fewer market makers willing to quote tight prices.

- Always include spread costs when you calculate break-even points for short-term trades or frequent rebalancing.

Introduction

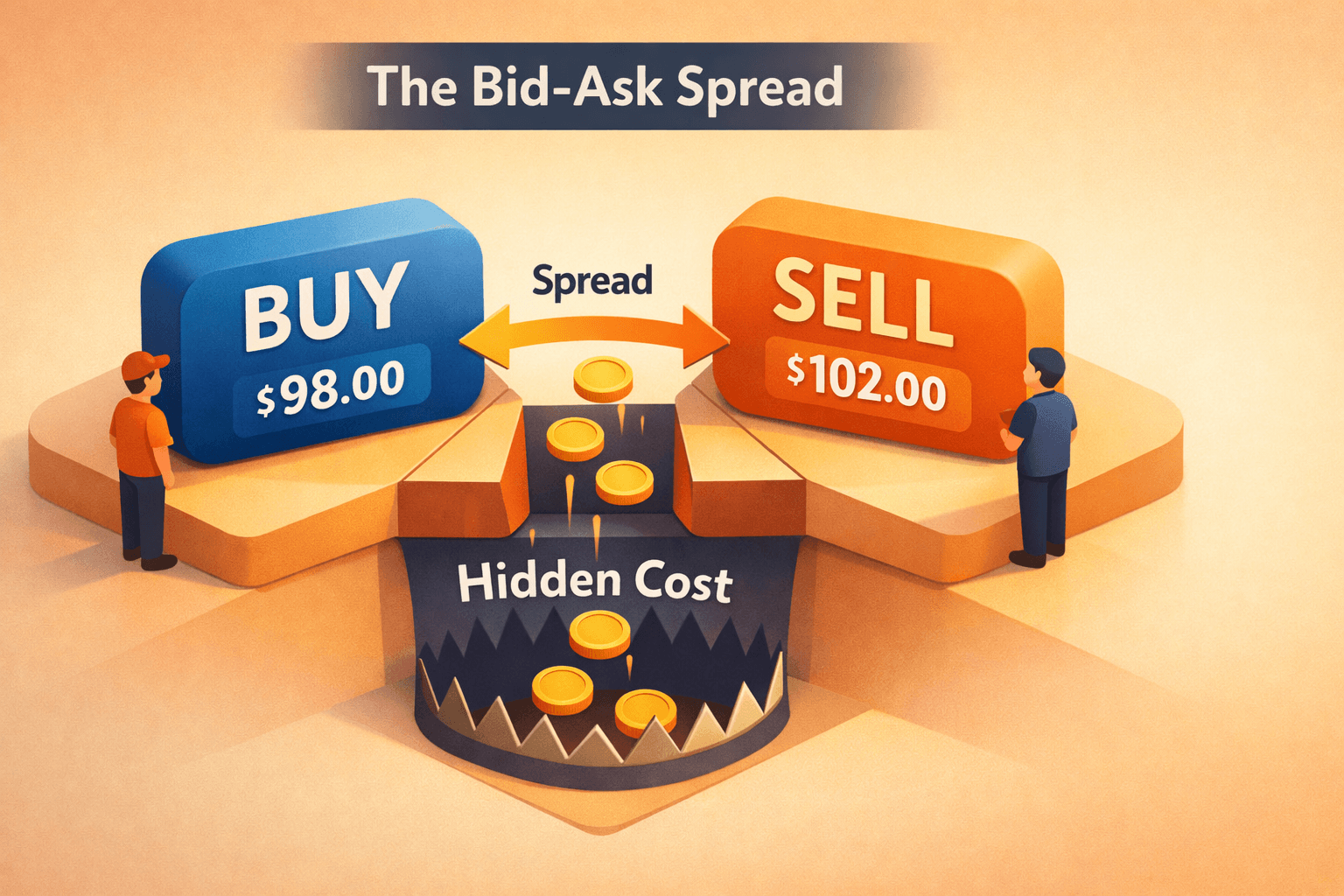

The bid-ask spread is the gap between the highest price a buyer is willing to pay, the bid, and the lowest price a seller will accept, the ask. This gap is a hidden but real cost each time you trade, and it affects how much you keep from a trade even before commissions or fees.

Why should you care about the spread? Because it reduces your starting position as soon as you execute a market order. If you buy with a market order, you pay the ask, and if you sell immediately you receive the bid. Have you ever wondered why you seem to lose a little right after buying a stock? The spread is often the reason.

In this guide you'll learn how spreads form, why they vary across securities and times of day, simple tactics you can use to minimize spread costs, and what spread patterns tell you about market sentiment. Along the way you'll see practical examples that show real numbers you can apply to your own trades.

What Is the Bid-Ask Spread?

The bid is the highest price buyers are willing to pay right now. The ask is the lowest price sellers are willing to accept right now. The difference between those two prices is the bid-ask spread, sometimes called the spread.

Spreads are usually quoted in dollars and cents for individual stocks. For example, if a stock shows a bid of 150.00 and an ask of 150.10 the spread is 0.10, or ten cents. For percentage-minded investors the spread divided by the mid-price gives you the relative cost.

Why the spread exists

Several market participants create and respond to bids and asks. Market makers and high-frequency traders post quotes to earn the spread by buying at the bid and selling at the ask. They take on inventory and execution risk, so they widen their quotes when uncertainty or risk rises.

At the end of the day, the spread compensates liquidity providers and balances supply and demand in real time. If no one is willing to buy near the ask, sellers either lower their price or wait, and the ask-bid gap can widen.

How Spreads Affect Your Trading Costs

Spreads are an implicit cost, different from explicit costs like commissions. You pay them automatically when you cross the spread with a market order. That reduces your effective entry price or exit proceeds immediately.

Simple examples

Example 1, a liquid large-cap. Suppose $AAPL shows a bid of 150.00 and an ask of 150.10. You buy 100 shares with a market order at 150.10, spending 15,010. If you immediately sell at the bid you receive 15,000. The spread cost is 10.00, about 0.067 percent of the trade value.

Example 2, a thinly traded small-cap. A small company trades at 5.00 with a bid of 4.80 and an ask of 5.20. Buying 1,000 shares at 5.20 costs 5,200. Selling immediately at the bid yields 4,800. The spread cost is 400, which is 8 percent of the trade value. That shows how wide spreads can crush short-term returns.

Why Spreads Vary: Liquidity, Volatility, and Market Structure

Not every security has the same spread. Several key factors explain why spreads differ across stocks and time periods. Understanding these helps you pick trading times and instruments that reduce cost.

Liquidity and trading volume

Liquidity refers to how easily a security can be bought or sold at stable prices. High-volume, large-cap stocks like $AAPL or $MSFT often have very tight spreads, sometimes a few pennies or a couple basis points. Lower-volume stocks have wider spreads because fewer buyers and sellers are willing to quote tight prices.

Volatility and news

When a stock's price is swinging wildly or important news arrives, traders widen their quotes to protect against adverse price moves between quote and execution. Spreads often widen before or after earnings announcements and around major macro events.

Time of day

Spreads tend to be wider during pre-market and after-hours trading because fewer participants are active. The first and last 30 minutes of the regular session can also be more volatile and see slightly wider spreads for some stocks, although overall liquidity is usually higher during regular hours.

Market structure and venue

Different trading venues and market maker obligations affect quotes. Some exchanges offer incentives for liquidity providers to post tight quotes, while other venues might fragment order flow and temporarily widen apparent spreads. Retail trading platforms aggregate quotes to show best bid and offer, but hidden orders and venue differences can still matter.

How to Minimize Spread Costs: Practical Order Tactics

You don't have to accept the spread as a fixed tax on every trade. You can use order tactics and timing to reduce spread costs. These methods are especially helpful if you're a frequent trader or working with small positions where every cent matters.

Use limit orders instead of market orders

Limit orders let you specify the worst price you will accept. If you place a buy limit at the bid you might get executed at or near the bid instead of paying the ask. That means you won't immediately cross the spread. The trade-off is execution risk, because your order might not fill if the market moves away.

Trade during regular market hours

Executing during regular trading hours often gives you the tightest spreads. If your strategy allows it, avoid pre-market and after-hours trades for small or illiquid stocks where spreads can be unpredictably wide.

Pick more liquid instruments for active strategies

If you plan to trade often, favor highly liquid ETFs or large-cap stocks. For example, the ETFs that track major indexes often trade with tight spreads and deep order books. That makes it cheaper and faster for you to get in and out.

Consider order size and price improvement

Large orders can move the market and face worse fills. Break bigger trades into smaller orders if you can, and look for price improvement features your broker might offer. Some brokers route orders to venues that provide better fills than the displayed ask or bid.

What Spread Patterns Tell You About Market Sentiment

Spreads are more than a cost. Changes in spread width and the behavior of bid and ask quotes give you a read on supply and demand and on trader confidence. You can use this information as part of a broader market analysis.

Widening spreads often signal uncertainty

When spreads widen quickly, that usually indicates fewer participants are willing to take the other side of trades. That can happen before earnings, during macro shocks, or when news creates asymmetric information. Wider spreads mean higher transaction risk and higher expected trading costs.

Tight spreads suggest balanced supply and demand

Consistently narrow spreads in a stock typically mean deep order books and active market making. That implies other traders are confident in fair pricing and willing to commit capital at close prices. Tight spreads make it easier for you to enter and exit without large slippage.

Asymmetric changes hint at directional pressure

Sometimes the bid moves lower while the ask stays similar, or the ask moves higher while the bid is steady. That asymmetry can show directional pressure. If bids fall, buyers are retreating. If asks climb, sellers are pushing prices up and you might be seeing early signs of a trend or a liquidity drain.

Real-World Examples: Numbers You Can Use

Here are two concrete scenarios that show how spread costs matter in real decisions you might make.

-

Short-term trade in a liquid stock. You plan to scalp $AAPL for a quick gain. The NBBO shows bid 150.00, ask 150.10. If your target profit is 0.20 per share, remember that buying at 150.10 and later selling at 150.20 gives only 0.10 of upside after crossing the initial spread. That cuts your expected profit in half, so you should either use a limit buy near 150.00 or target larger price moves.

-

Rebalancing a small account with an illiquid position. You hold a small-cap stock trading around 5.00 with a 4.80 bid and 5.20 ask. Rebalancing by selling immediately at the bid costs you 8 percent of the position value. If your portfolio is small, those spread costs can wipe out the benefits of diversification. Consider limit orders or waiting for better liquidity.

Common Mistakes to Avoid

- Using market orders all the time: Market orders cross the spread and guarantee cost. Use limit orders when you can accept potential non-execution.

- Ignoring spread in cost calculations: Some traders count commissions but forget the spread. Always include the spread when calculating break-even points for short-term trades.

- Trading illiquid stocks around news: Spreads often widen into and after news, turning a small expected move into a net loss. Wait for liquidity to return or use cautious limit pricing.

- Assuming spreads are constant: Spreads change by time of day, volatility, and market events. Check quotes right before you trade, not from memory.

- Overtrading small accounts: Frequent trades magnify spread costs. At the end of the day, less can be more for small portfolios.

FAQ Section

Q: What is the difference between spread and slippage?

A: The spread is the displayed gap between bid and ask at a moment in time. Slippage is the difference between the expected price and the actual executed price. Crossing the spread with a market order produces immediate slippage equal to the spread, but slippage can also occur if the price moves while your order is filling.

Q: Do commissions still matter if spreads are wide?

A: Yes, both matter. Commissions are explicit costs while spreads are implicit. Wide spreads can dominate small commissions, but you should include both when estimating total trading cost.

Q: Can my broker get me better than the displayed price?

A: Sometimes yes. Brokers may achieve price improvement by routing your order to venues that offer better execution. However, improvement is not guaranteed, and it varies by broker and order type.

Q: Are spreads the same in ETFs and stocks?

A: Not necessarily. Many large ETFs have tight spreads similar to blue-chip stocks because authorized participants keep supply matched to demand. But niche or leveraged ETFs can have wider spreads, especially if underlying markets are less liquid.

Bottom Line

The bid-ask spread is a fundamental but often overlooked trading cost that matters for both beginners and active traders. Spreads are smallest in liquid, high-volume securities and can be large in thinly traded or volatile situations. You should treat the spread as part of your trading plan and cost calculations.

Take practical steps to reduce spread costs: use limit orders, trade during normal hours, prefer liquid instruments for frequent trading, and size orders thoughtfully. Watch spread patterns for clues about market sentiment, and always include the spread when you calculate break-even levels for short-term strategies.

Start by checking spreads on the securities you trade this week. Try placing a limit order at a competitive price to see how often you get filled. Over time you will get a feel for when the spread is a minor annoyance and when it becomes a material cost.